Invest with FHSA

Start Saving For a Down Payment Today

The First Home Savings Account (FHSA) is a type of registered savings plan introduced by the federal government in 2022. An FHSA is designed to help you save for your first home, tax-free and help you reach your vision of owning a home faster!

Looking for advice?

We can help.

or call (647)323-3231

What is a FHSA?

Saving for your first home just got easier.

The First Home Savings Account (FHSA) is a registered savings account designed to help Canadians save for their first home. The FHSA combines features of an RRSP and TFSA, offering tax-deductible contributions and tax-free withdrawals for qualifying expenses. This new savings vehicle can hold various investment types to help your money grow tax-free.

Who Qualifies?

To open a First Home Savings Account, you must be:

- A Canadian resident

- 18 years or older

- A first-time home buyer

An individual is considered to be a first-time home buyer if at any time in the part of the calendar year before the account is opened or at any time in the preceding four years they did not live in a qualifying home (or what would be a qualifying home if located in Canada) that either they owned or their spouse or common-law partner owned (if they have a spouse or common-law partner at the time the account is opened).

FHSA vs. Other Plans

How is the FHSA different from the Home Buyers’ Plan?

With the current Home Buyers’ Plan, Canadians can withdraw up to $60,000 from their RRSP subject to eligibility and conditions. The funds must be paid to the RRSP over 15 years.

With an FHSA, eligible withdrawals do not need to be paid back.

Comparing FHSA with RRSP and TFSA

The FHSA is a registered plan that combines certain features of both RRSP and TFSA, designed to assist you in saving for your first home purchase!

| FHSA | RRSP | TFSA | |

|---|---|---|---|

|

How does this plan help me? |

Investing with contributions and using them to purchase a first home. |

You can borrow up to $35,000 from your existing RRSP, but the borrowed funds must be paid back within 15 years. |

Invest with contributions, enjoy tax-free returns, and use the funds to purchase a home. |

|

What are the contribution rules? |

The annual contribution limit is $8,000. The individual’s lifetime contribution limit is $40,000. |

Contribute the lower of 18% of your previous year’s income or the current fixed contribution limit of $30,780 for 2023. There is no lifetime contribution limit. |

The annual contribution limit for 2024 is $7,000, and the limit is cumulative. Click to learn more. |

|

Is it eligible for tax deductions? |

Eligible contributions are tax-deductible, excluding funds transferred from RRSP to FHSA. |

Eligible contributions are tax-deductible (except on transfers into your RRSP from your FHSA). |

Contributions are not eligible for tax deductions. |

|

Key advantages |

Invest with the funds in the account, and profits are tax-free. Additionally, you may be able to transfer funds tax-free from FHSA to RRSP or RRIF. |

Funds can be used to purchase a qualifying home through the HBP. Investment profits within the plan are tax-deferred. |

The funds in the account can experience tax-free growth and can be utilized for various expenses, including homeownership. |

|

Limitation Terms |

The ownership period of the FHSA ends on the earliest of the following dates: the 15th anniversary of opening your first FHSA account, the December 31 of the year you turn 71, or the year following the first eligible withdrawal. Non-qualifying withdrawals (withdrawals not used for the purchase of a qualifying home) are considered taxable income. |

According to the HBP plan, any RRSP withdrawal used to purchase or build a qualifying home must be repaid to your RRSP within 15 years, starting from the second year following the year of your initial withdrawal. Failure to repay the required amount within the specified timeframe will be treated as taxable income for that year. |

Contributions made to a TFSA are not eligible for tax deductions. |

Contribute and Withdraw

Make the most of your FHSA by contributing regularly and growing your savings. Here’s an overview of the rules for contributing and withdrawing funds from your FHSA, as outlined by the Government of Canada.

You must use your FHSA contributions within 15 years of opening the account, or by the time you turn 71 years old, whichever is sooner. After that time, you can transfer savings into an RRSP or RRIF or make a taxable withdrawal.

If you qualify to use your savings towards the purchase of a qualifying home, you can withdraw money from your FHSA, tax-free. For the same home purchase, you may also be able to withdraw money from your RRSP Home Buyers’ Plan.

What types of products can be held in a FHSA?

Let your money bring your goals closer

Despite its name, it’s not a typical savings account – it’s a place where you can put investments like segregated funds.

By leveraging the tax-free growth advantage of an FHSA, you have up to 15 years to invest and benefit from compound growth.

Returns will, of course, vary depending on the financial market and the investment vehicles you choose. But generally speaking, the sooner you start contributing, the higher your FHSA returns will be.

Ai Financial offers this investment opportunity:

Segregated Funds

Segregated fund policies give you the freedom to invest while offering insurance protection to preserve your savings. With our choice of guarantees, you can expand your wealth and secure it at the same time.

You can purchase Segregated Funds using various accounts, including but not limited to TFSA, RRSP, RESP, Non-Reg, etc.

Why do we encourage you to invest in an FHSA as early as possible?

The FHSA allows you to hold funds in the account for up to 15 years, during which time your initial contributions can grow into a substantial amount for purchasing a home.

At Ai Financial, our historical investment returns have successfully doubled our clients’ assets within five years.

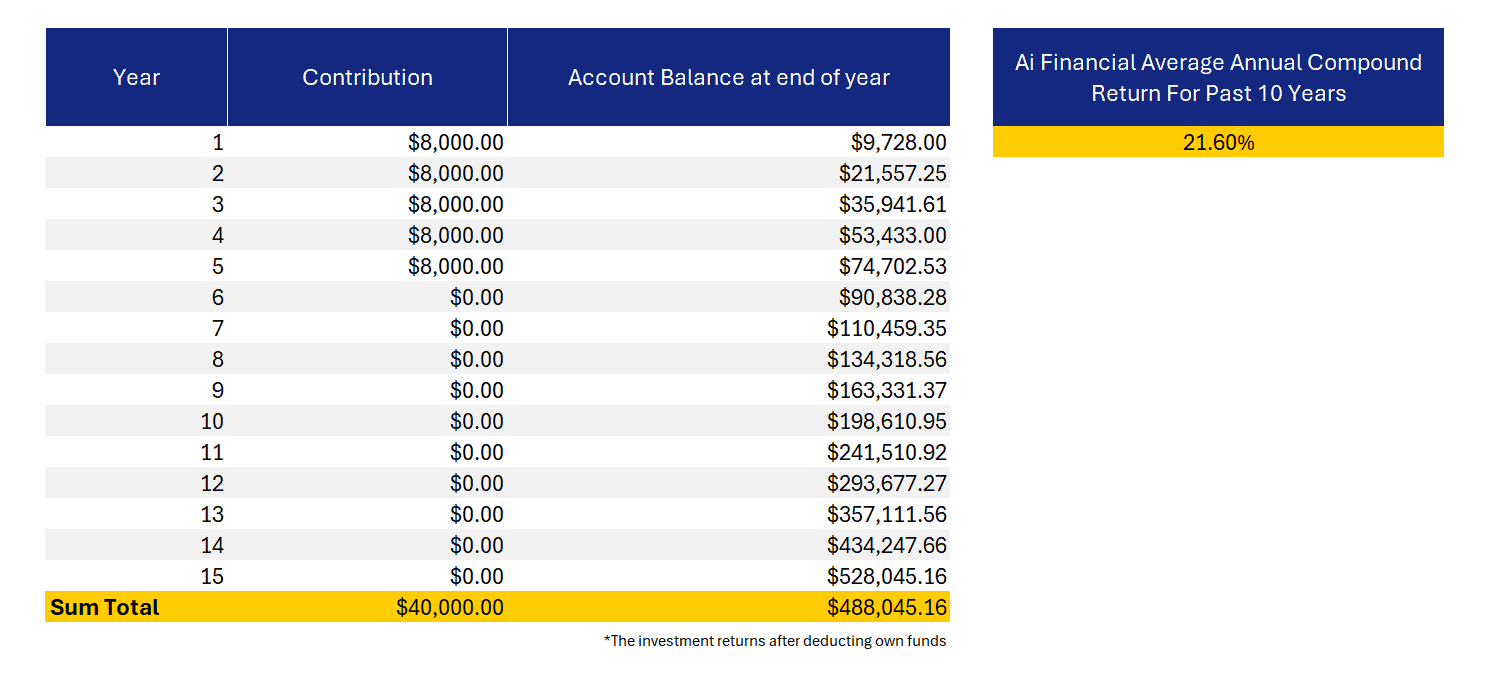

Let’s simulate how much financial support your could potentially receive within 15 years based on our historical investment returns:

If you max out your TFSA contribution limit every year, you have the opportunity to achieve tax-free investment gains of $480,000 after 15 years based on Ai Financial’s historical average annual return of 21.6% (excluding the initial $40,000 principal). This would provide substantial support for a down payment on a new home.

Maybe you’re concerned about our return rate accuracy, using the historical average annual return of the SPY 500 (approximately 15%), you could still achieve investment gains of $210,000 after 15 years. If you have a spouse, doubling your contribution room and returns can effectively help alleviate the pressure of buying a home.

You may also want to explore other accounts...

What's the safest way to invest in Canada? RRSP + Segregated Funds

The three most important investment principles are: first, preserve your capital; second, preserve your capital; and third, remember the first and second principles.

To some extent, RRSP is worth purchasing. It offers short-term tax benefits and long-term financial support for retirement. However, from the time of purchasing RRSP to using it in old age, there are decades in between. How should you manage or invest your RRSP account during this period? How can you ensure that the returns on your RRSP investments will truly serve your retirement needs? This raises the question of ensuring the security of RRSP investments.

Combining RRSP with Segregated Funds>>>

PAD with TFSA - Grow Your Funds Automatically, Efficiently, and Effortlessly

A pre-authorized debit allows the biller to withdraw money from your bank account when a payment is due. Pre-authorized debits may be useful when you want to make payments from your account on a regular basis. On the specified deduction dates, the distributor automatically deducts the predetermined amount from the investor’s designated bank account and executes the purchase of the chosen fund.

By setting up a dollar-cost averaging plan with Ai Financial, you can schedule regular deductions from your bank account into your designated investment account (TFSA/RRSP/RESP/Non-Registered, etc.) on a weekly, bi-weekly, or monthly basis. Once you initiate this regular investment strategy, the long-term appreciation of your funds is likely to pleasantly surprise you.

More Canadian Investment Guides >>>

Resources

What is an investment loan?

Can this loan last a lifetime? Interest-only payments? Tax-deductible? Is it a private loan? Is the threshold high?