TFSA withdrawal rules and limits

Key takeaways

- Tax-Free Withdrawals: Withdrawals from TFSA are tax-free unless you’re actively day trading.

- Contribution Rules: You can recontribute withdrawn amounts in the following calendar year, based on your contribution room.

- Flexible Withdrawals: You can withdraw from TFSA anytime with no limits on frequency or amount.

- Investment Advantage: TFSA is ideal for both short-term needs and long-term investment growth.

What’s in this article?

Why open a TFSA?

Among many other benefits, tax-free withdrawals are a key advantage TFSA offer. They’re a great place to hold mutual funds, segregated funds, or other kinds of investments.

TFSA can fit both short-term and long-term financial goals. While commonly used to save up for purchases like a house or vacation, TFSA can also be a place to put your investments to prepare for retirement. Plus, given the name, your money can grow tax-free.

Given this flexibility, TFSA are an option for those wanting the freedom to use the money at any time. Keep in mind that for RRSPs and other registered accounts, withdrawals are taxed, making TFSA the more viable option for shorter-term goals. When it comes time to use the money in your TFSA, there are a few rules to keep in mind. Check out the guidelines below to ensure you’re informed on the withdrawal process.

How to withdraw from a TFSA

What happens when I withdraw money from my TFSA?

Withdrawing money from your TFSA doesn’t have to be permanent—you can recontribute this amount in future years. This flexibility allows you to use TFSA funds for big purchases like a car, home, or emergency expenses.

Before making a withdrawal, it’s essential to understand your contribution and recontribution limits. If you’ve already maxed out your contribution room (the amount you’re allowed to add to your account), you must wait until the following calendar year to add any funds you’ve withdrawn.

For example, let’s say Jamie opens a TFSA in 2023 and deposits $4,500. With the 2023 contribution limit set at $6,500, Jamie has $2,000 remaining in contribution room. In 2024, Jamie’s contribution room will include the new annual limit plus the $2,000 unused from the previous year.

If Jamie decides to withdraw $1,000 from the TFSA in 2024, this amount will be added to the recontribution room for the next year. This means Jamie can only recontribute the additional $1,000 to the TFSA in 2025, the year after the withdrawal.

By calculating your total contribution room, you can better manage how much you’re able to contribute after making a withdrawal.

What is the TFSA limit?

| Year | Limit |

|---|---|

|

2009 to 2012 |

$ 5,000 |

|

2013 and 2014 |

$ 5,500 |

|

2015 |

$ 10,000 |

|

2016 to 2018 |

$ 5,500 |

|

2019 to 2022 |

$ 6,000 |

|

2023 |

$ 6,500 |

|

2024 |

$ 7,000 |

- The annual TFSA contribution limit for 2024 is $7,000.

- Your contribution limit starts the year you turn 18 and TFSA’s were introduced in 2009.

- If you didn’t contribute to a TFSA between 2009 and 2024 and you were at least 18 in 2009, your total contribution limit could be $95,000.

- You can carry forward any unused contribution room from previous years.

- If you contribute more than your total contribution room, the Canada Revenue Agency (CRA) will charge you a penalty of 1% per month on the excess amount.

Is there a limit on how much I can withdraw?

No, for TFSA, there’s no rule on how much you can withdraw. But remember that after you withdraw, you can only recontribute that amount the following year. Take your total contribution room into consideration when planning your withdrawal.

When can I withdraw my money?

You can withdraw from a TFSA at any time. The longer you leave your money in the account, though, the more your investments have a chance to grow. You can earn more through the compounding effect (your interest will gain interest).

How many times can I withdraw money?

You’re allowed to withdraw money as many times as you want; there are no limits.

Will I Be Taxed on the Amount I Withdraw?

According to the Canada Revenue Agency (CRA), withdrawals from your TFSA are not taxed as long as you are not engaging in day trading or conducting business activities. The CRA typically flags accounts based on the frequency of transactions, types of shares, and your knowledge of the securities markets. Qualified investments for a TFSA include stocks, bonds, savings accounts, and mutual funds.

TFSA is designed for long-term financial growth, not for frequent trading. If you frequently trade within your TFSA, any gains might be subject to taxation.

If you’re unsure whether this applies to you, refer to the table below. These are the factors the CRA uses to determine if a TFSA account will be taxed. While these factors serve as a benchmark, remember that there is no definitive rule on the number of trades that constitute excessive trading.

Do I have to re-invest what was withdrawn?

No, you have no obligation to re-invest the money you withdrew.

A Small Reminder about Setting Up Your Spouse as the beneficiary of TFSA

Many people designate their spouse as the beneficiary of their TFSA account. However, this is not the best option. When a spouse is named as the beneficiary, the account loses its TFSA status upon transfer and becomes a regular account. Instead, designating your spouse as the Successor Holder ensures they inherit both the funds and the TFSA’s tax-advantaged status. Only spouses can be named as Successor Holders.

For example, consider a couple who have each maximized their TFSA limits, with $80,000 in each account. If the husband passes away, the wife, as a beneficiary, would receive the funds but would need enough TFSA room to keep the money in a TFSA. If her TFSA room is also full, the funds would go into a regular account, and future earnings would be taxable.

However, if the wife is the Successor Holder, she can inherit the husband’s TFSA without affecting her own TFSA room. The account retains its TFSA status, and future withdrawals remain tax-free.

Thus, it’s better to designate your spouse as the Successor Holder, not as a Beneficiary, to fully utilize the benefits of a TFSA.

Common Misconceptions About Using a TFSA

Misconception: TFSA Contribution Room Only Increases

Many people believe that TFSA contribution room only increases because unused room carries forward to future years, and the government adds new contribution room annually. Some even accumulate substantial funds in their TFSA accounts through investments.

However, TFSA contribution room can decrease if your investments perform poorly. Continuous losses can shrink your contribution room, and in extreme cases, it can reduce to zero. For example:

A few years ago, cannabis stocks were extremely popular with impressive gains. Imagine someone used their TFSA to buy $57,500 worth of CGC stock in early 2020, totaling 2,400 shares. By early 2021, their account could be worth $100,000. Feeling optimistic, they might decide to hold onto the stock, expecting further gains. Unfortunately, if the stock price plummets and their TFSA account balance drops to $6,000, they may decide to cut their losses and withdraw the remaining funds. In this case, the TFSA contribution room would shrink due to the losses from the stock sale.

If an even more extreme situation occurs and the TFSA funds are invested in a stock that goes bankrupt and becomes worthless, the contribution room in that TFSA account would effectively become zero.

Therefore, when using a TFSA for investments, it’s crucial to choose solid investment options. Otherwise, attempting to stop losses may lead to even greater losses. Selecting the right investments allows for long-term holding without the fear of incurring losses, thus preserving both your assets and your TFSA contribution room.

How to Maximize Your TFSA Account

After understanding the misconceptions surrounding TFSA accounts, it’s crucial to highlight another essential aspect: TFSA is more than just a savings account. To fully leverage the advantages of a TFSA account, it’s essential to choose a sound investment strategy. Here are a few strategies to consider:

Strategy 1: Coordination with Other Accounts

To maximize TFSA contributions annually, you might need to overcome financial constraints. Here are some practical approaches:

Using HELOC with Home Equity

If you own a home, you can leverage your home equity through a Home Equity Line of Credit (HELOC) to contribute to your TFSA. If the investment returns in your TFSA exceed the interest on the HELOC, this strategy can effectively create wealth.

Using RRSP Tax Refunds

Another common method is utilizing tax refunds from RRSP contributions. Before filing taxes each year, contribute to an RRSP and use the tax refund to fund your TFSA. This approach optimally utilizes both accounts. If funds are not available in your RRSP, consider applying for an RRSP loan, which typically offers competitive interest rates around prime plus 0.5%. For personalized planning, consult a financial advisor.

Strategy 2: Leveraging Combined Investment Approaches

This advanced TFSA strategy involves combining TFSA contributions with investment loans to maximize returns. Here’s how it works:

Investment loans focus on long-term value investing with the power of compounding. Over time, assets accumulated in non-registered accounts can grow significantly. When a substantial sum is withdrawn in the future, only 50% of the capital gains are taxable as Capital Gains. However, there’s a way to potentially avoid this tax.

This is where the TFSA comes into play. Suppose you withdraw the annual TFSA contribution limit of $6,000 from the profits of your investment loan each year. The amount withdrawn is taxable at that time but typically incurs minimal taxes due to the small base. Once deposited into your TFSA, any future appreciation is entirely tax-free. With a well-chosen investment, the long-term growth potential can be remarkable.

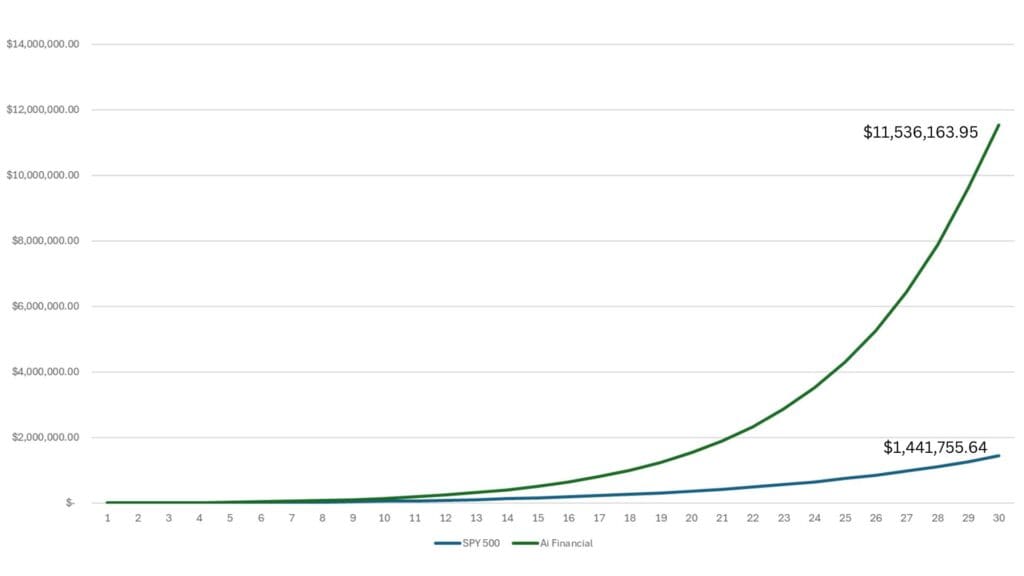

The chart below illustrates the returns of the S&P 500 Index and AiF over 30 years, showing potential outcomes:

Disclaimer: This chart is for demonstration purposes only and does not represent any investment commitment.

From the chart, leveraging a TFSA with annual $6,000 investments over 30 years can lead to significant wealth accumulation. Even with a conservative estimate of a 12% return from the S&P 500, the TFSA could grow to over $1.5 million. Using an average annual compound return of 21.6% from AiF, it could reach $2 million in approximately 21 years, making it a substantial income source for a comfortable retirement. Withdrawals from a TFSA, even reaching millions, are tax-free.

This demonstrates the power of tax-free growth in a TFSA account. The key is making informed investment decisions! Need guidance on making these “correct” investments?

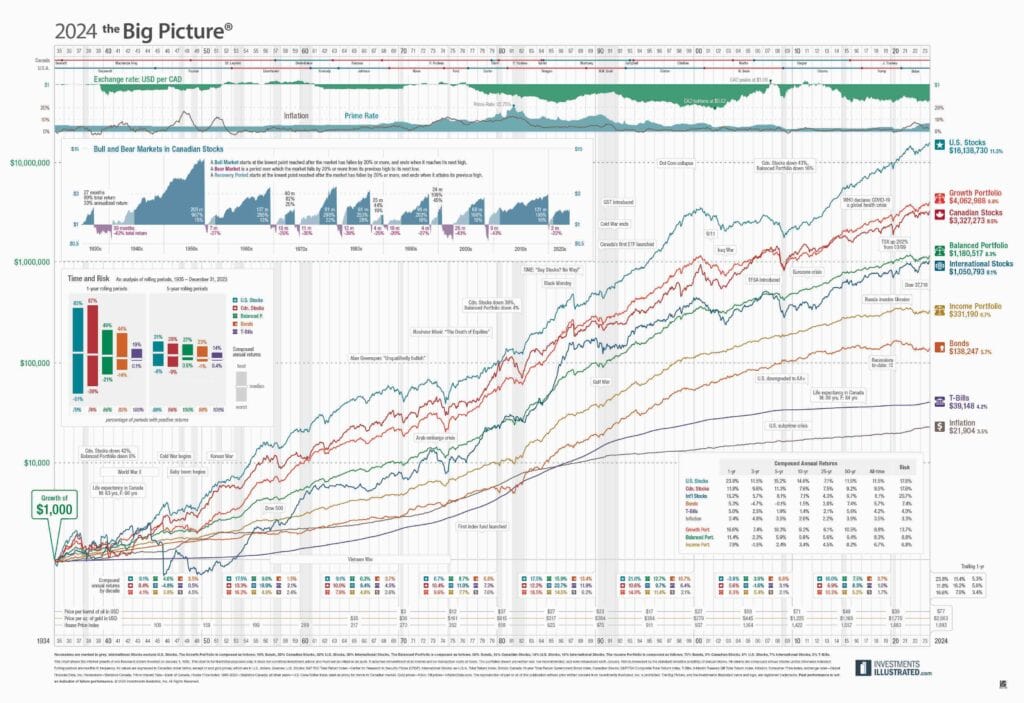

Let’s take a look at this comprehensive market trend chart:

This chart illustrates the long-term trends of different markets. If someone had invested $1,000 in 1934 (starting point in the bottom-left corner) in the U.S. market (the top line on the chart), by the end of 2021, their investment would have grown to $14,861,397, a staggering increase of 14,861 times. Similarly, investing in the Canadian market would have yielded $3,162,135, a growth of 3,162 times. These figures reflect the growth in the North American markets over time.

In essence, if you invest your TFSA funds aligned with these market trends, significant returns are virtually guaranteed.

To sum up, it’s crucial to manage your TFSA as an investment account, requiring strategic planning starting from now. As a saying in the investment world goes, “The best time to invest was 10 years ago; the second-best time is now.” Therefore, start investing wisely and capitalize on the potential growth opportunities available through your TFSA.

What's next?

How much money you choose to withdraw will depend on your intended use.

Once you’ve decided on your withdrawal amount, taking your contribution limits into consideration, you can transfer the money online.

Meet with an advisor to learn how a TFSA can best meet your needs.

You may also interested in

What is an investment loan?

Can this loan last a lifetime? Interest-only payments? Tax-deductible? Is it a private loan? Is the threshold high?

RRSP withdrawal rules

RRSP can be effective vehicles to save for retirement; but making withdrawals from these tax-advantaged……