Investment Accounts in Canada | What are they and how to use

Canadian residents enjoy benefits from various registered account, such as tax deferral with RRSPs, tax-free growth with TFSAs, and new accounts like FHSAs. How can you effectively use these accounts to maximize benefits and achieve both profit and tax savings? This article will comprehensively introduce common Canadian investment and savings accounts, their usage, common pitfalls, and suitable investment products.

What’s in this article?

Investment Accounts

RRSP - Registered Retirement Savings Plan

The Registered Retirement Savings Plan (RRSP) is a Canadian account designed for saving and investing. It offers taxpayers significant control within government-set rules. The two main advantages of RRSPs are:

- Annual RRSP contributions can reduce income taxes for that year.

- RRSPs help high-income earners defer taxes.

Opening an RRSP account is easy through financial institutions like banks, investment companies, and trust companies. Contributions can be made monthly, annually, or as a lump sum.

Eligibility requirements include having earned income, a social insurance number, having filed taxes, and being under 71 years old. If you are over 71, you can still benefit by contributing to a spousal RRSP if your spouse is under 71.

RRSPs can serve both short-term and long-term financial goals.

Short-Term Goal: Tax Refunds

The Registered Retirement Savings Plan (RRSP) was introduced by the Canadian government in 1957 to encourage saving during working years, providing income during retirement for a comfortable life. The government offers tax benefits as an incentive.

Key points about RRSP:

- It requires an account to be opened.

- Contributions can be made by the individual, their spouse, or common-law partner.

- Money in an RRSP can reduce taxable income, lowering the tax bracket and providing tax deferral. However, withdrawals may be taxable.

Why does the government provide these benefits? Simply put, to ensure Canadians save for retirement and reduce reliance on public funds.

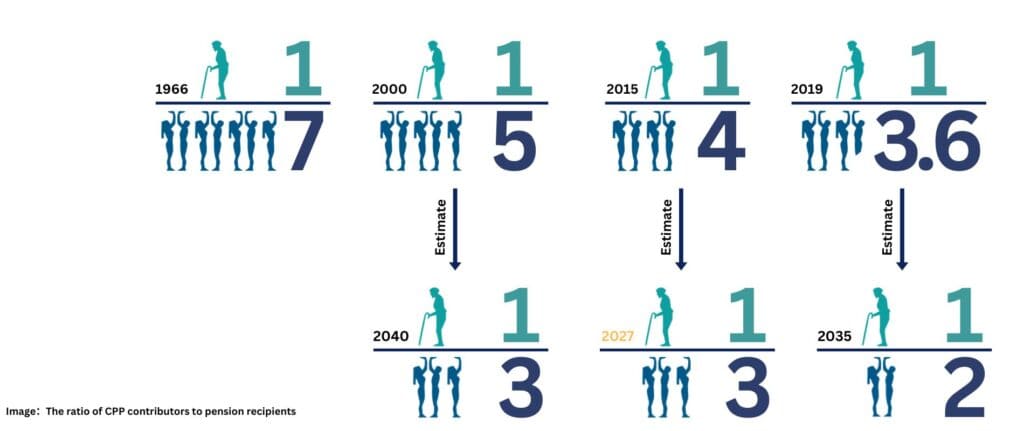

Historical CPP Contributions vs. Pension Recipients

- 1966: When the CPP was established, the ratio 7.7 working-age individuals for every senior

- 2000: The ratio was 5 working-age individuals for every senior, with a projection of 3:1 by 2040.

- 2015: The ratio was 4 working-age individuals for every senior, reaching the 3:1 by 2027, 13 years earlier than previous estimation.

- 2019: The ratio was 3.6 working-age individuals for every senior, with a projection of 2:1 by 2035.

Currently, there are 3.4 working-age individuals for every senior (2022). This is expected to decrease to 2:1 by 2035, indicating an accelerating trend.

Longevity and Quality of Retirement

Advancements in medical care, wellness products, healthy diets, exercise, and cosmetic procedures have significantly increased human lifespan. With more elderly individuals aiming for a high-quality retirement, the pressure on the working population to support them increases. How can we ensure a comfortable retirement under these circumstances?

Measures to Address the Decline in Support Ratios

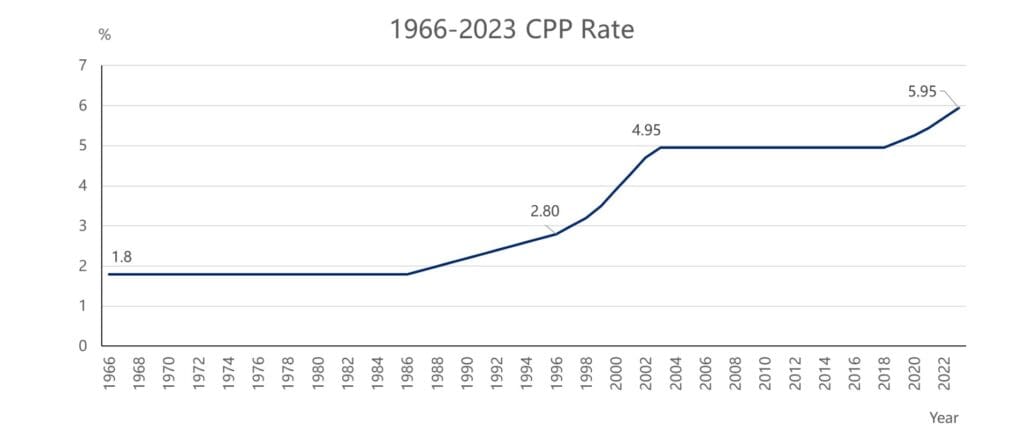

To slow the decline in the worker-to-retiree ratio, the government has implemented various measures, notably increasing the CPP contribution rate. The historical trends of CPP rates from 1966 to 2023 are as follows:

- 1966-1986: CPP rate remained at 1.8%.

- Late 1980s: CPP crisis led to an annual increase of 0.1%.

- 1998: Worsening crisis prompted varying annual increases.

- 1999: Establishment of the CPP Investment Board (CPPIB) to manage investments.

- 1999-2003: Due to successful CPPIB investments, the rate stabilized at 4.95%.

- 2019: Rising concerns about CPPIB’s sustainability led to gradual increases again.

- 2023: The rate reached 5.95%, indicating that investment returns alone couldn’t solve the issue.

The Importance of Personal Retirement Planning

This trend highlights the growing strain on national pensions. If retirees don’t plan their finances well, the burden will fall on their children, who will face higher CPP contributions.

Purchasing an RRSP is a long-term strategy to ensure a comfortable retirement and support the government’s efforts. It also helps reduce the financial burden on our children.

Types of RRSPs

There are three common types of RRSPs: Individual RRSP, Spousal RRSP, and Group RRSP. Here are their features:

1.Individual RRSP

- This is an RRSP account opened in the individual’s name.

- It is the most common form of RRSP, ideal for salaried individuals.

- Contributions should be within the allowable limit; exceeding this limit incurs a 1% monthly penalty from the government.

- Like other registered accounts, Individual RRSPs have contribution limits set by the CRA.

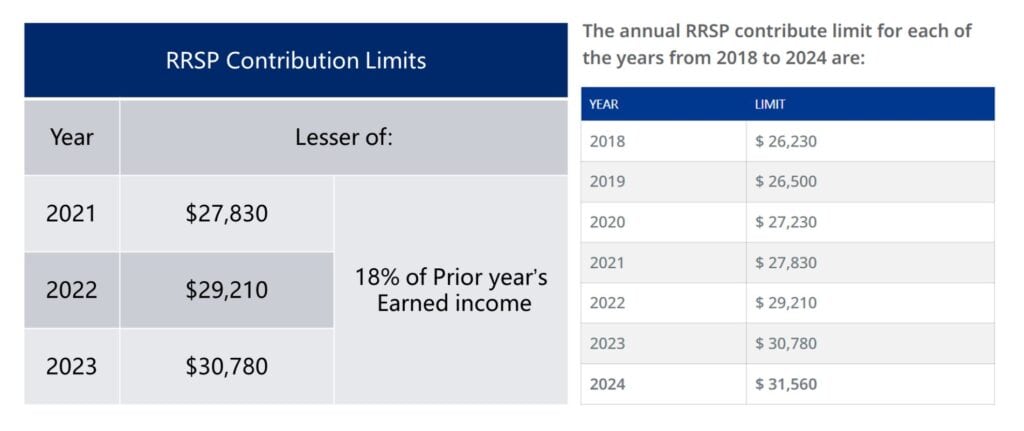

The formula for calculating the annual RRSP contribution limit is:

RRSP Growth = Previous Year’s Earned Income x 18%

For example, if you reported an income of $100,000 in 2022, your 2023 RRSP contribution limit would be $100,000 x 18% = $18,000. This means your RRSP limit increases by $18,000 for 2023. However, there is an annual maximum contribution limit set by the government.

For instance, in 2023, the maximum RRSP contribution limit is $30,780. So, even if your calculated limit based on earned income exceeds this amount, you can only contribute up to $30,780. If your earned income is $200,000, the formula yields $36,000, but you are capped at $30,780.

Accumulating RRSP Contribution Room

Unused contribution room from previous years can be carried forward and used in future years. Contributions can be made monthly, annually, or at any time within the limit.

2. Spousal RRSP

The Spousal RRSP is ideal for couples with significant income differences, as it helps reduce their overall tax liability. This type of RRSP is suitable when one spouse earns substantially more than the other. For example, if the husband earns $150,000 and the wife earns $40,000, and the husband uses his RRSP contribution room to purchase a Spousal RRSP for his wife, this account is considered a Spousal RRSP.

However, there is a restriction: withdrawals from the Spousal RRSP cannot be made within three years. If funds are withdrawn within this period, they are taxed as the husband’s income. After three years, withdrawals are taxed as the wife’s income.

3. Group RRSP

A Group RRSP is a retirement benefit provided by employers to their employees. Many large organizations in Canada, such as government agencies and major banks, offer this benefit.

Participating in a Group RRSP allows your employer to match a portion of your contributions, which counts toward your RRSP contribution room. Companies often set a matching limit, such as a 1:1 ratio (you contribute 4%, and the company matches 4%) or a 1:0.5 ratio (you contribute 4%, and the company adds 2%).

Investment options are typically limited, with little personal involvement. Employees usually complete a questionnaire to determine their risk tolerance but have minimal control over investment choices. Additionally, while employed, you cannot transfer your Group RRSP; it is locked in (known as a Locked-in RRSP) and can only be moved to a Locked RRSP account after leaving the company.

These three types of RRSPs all use your personal contribution room. Whether you contribute to your own RRSP, a spousal RRSP, or a Group RRSP, all contributions count against your RRSP limit. Exceeding this limit results in a monthly penalty of 1% on the excess amount paid to the government.

TFSA - Tax-Free Savings Account

First, congratulations! Opening a TFSA (Tax-Free Savings Account) is very easy. Anyone aged 18 or older with a valid Social Insurance Number (SIN) can open an account. This includes international students with study permits, workers with work permits, and Canadian PR or citizens.

You can use a TFSA for various investments, including Segregated Funds, mutual funds, ETFs, stocks, and bonds. While the principal deposit is not tax-free, any earnings—such as capital gains, interest, and dividends—are completely tax-free.

The Canadian government sets an annual contribution limit for each individual. In 2023, eligible Canadian residents can contribute up to $6,500 to their TFSA. Contribution limits may vary each year. Here are the limits from previous years:

| Year | Limit |

|---|---|

|

2009 to 2012 |

$ 5,000 |

|

2013 and 2014 |

$ 5,500 |

|

2015 |

$ 10,000 |

|

2016 to 2018 |

$ 5,500 |

|

2019 to 2022 |

$ 6,000 |

|

2023 |

$ 6,500 |

|

2024 |

$ 7,000 |

Important Notes on TFSA Contribution Limits

- Any unused TFSA contribution room can be carried forward to the next year.

- If you turned 18 in 2009 or earlier, your TFSA contribution room increases annually, even if you haven’t filed income taxes or opened an account.

- If you turned 18 after 2009, your TFSA room accumulates starting from your 18th birthday.

- Investment earnings and value changes in your TFSA do not affect your current or future contribution limits.

- Notably, the principal growth and withdrawals from a TFSA do not impact your eligibility for government benefits, such as Ontario pensions, low-income subsidies, or federal tax credits.

- Most importantly, do not exceed your contribution limit; doing so incurs a 1% monthly penalty on the excess amount from the CRA.

- You can check your specific TFSA contribution limits by logging into your CRA account.

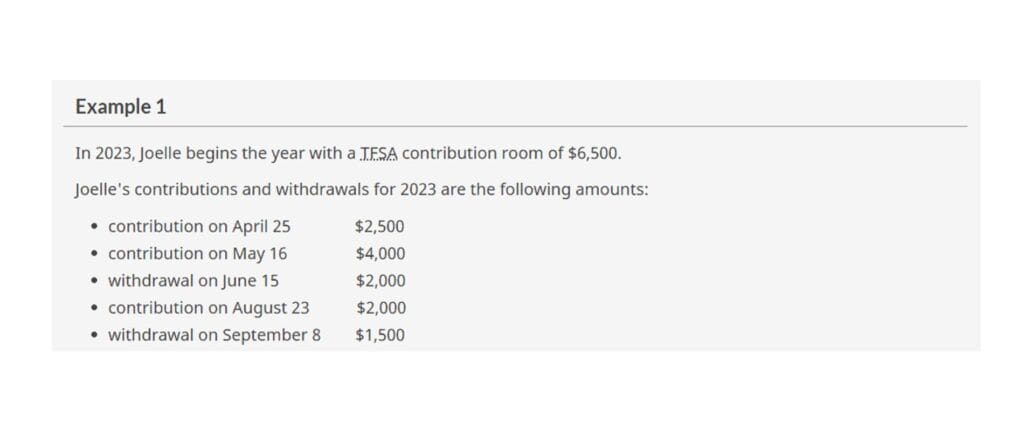

TFSA Contribution Example

According to a case provided by the CRA:

Joelle’s contributions in April and May exhausted her 2023 TFSA contribution room. Since her June withdrawal will not be added back until the following year, her contribution in August resulted in an excess of $2,000. In September, she withdrew $1,500, which will be considered for calculating her maximum excess TFSA amount in October. The remaining excess of $500 will carry over to the end of the year, leading to a 1% monthly penalty from August to December.

Tax Calculation:

- For August and September, the maximum excess amount is $2,000. The monthly penalty is $40 ($2,000 × 1% × 2 months).

- For October to December, the maximum excess amount is $500. The monthly penalty is $15 ($500 × 1% × 3 months).

Joelle’s withdrawals will be added to her TFSA room in early 2024.

How to Check Your TFSA Contribution Room:

- CRA Website: Log in to your account at www.cra-arc.gc.ca and follow the prompts to check your TFSA limit.

- Notice of Assessment (NOA): This document, received after filing taxes, clearly indicates your TFSA usage.

- Call the CRA: You can call 1-800-959-8281; have last year’s tax information ready for inquiries.

- Consult Your Accountant: If you use an accountant for taxes, they can provide information about your TFSA limit.

Another key advantage of a TFSA is the ease of withdrawals. Funds in a TFSA can be accessed anytime, but any contribution room created by withdrawals cannot be used in the same year; it becomes available again only in the following year.

RESP - Registered Education Savings Plan

RESP (Registered Education Savings Plan) is a government-developed initiative designed to help fund higher education for beneficiaries—youth under 17 who are studying. By contributing to an RESP, parents (subscribers) can save significantly on tuition costs due to interest earnings and government grants.

Having an RESP account ensures a secure financial future for your child’s education. As parents, we can cut costs in many areas, but education should never be compromised.

Important Considerations for RESP Investment

To apply for an RESP, the beneficiary must:

- Be a Canadian resident under 17 years old.

- Have a Social Insurance Number (SIN).

- Be preparing to enroll in an eligible post-secondary program that requires funds from the RESP.

If the beneficiary decides not to pursue higher education, the subscriber can:

- Transfer the RESP to another sibling.

- If the subscriber or their spouse has RRSP contribution room, transfer funds to an RRSP.

- Avoid withdrawing funds prematurely; the RESP can remain active for up to 35 years.

If withdrawals are made, the government grant portion must be returned, and earnings are subject to tax plus a 20% penalty. Some RESP plans may have additional restrictions, so it’s advisable to inquire when opening the account.

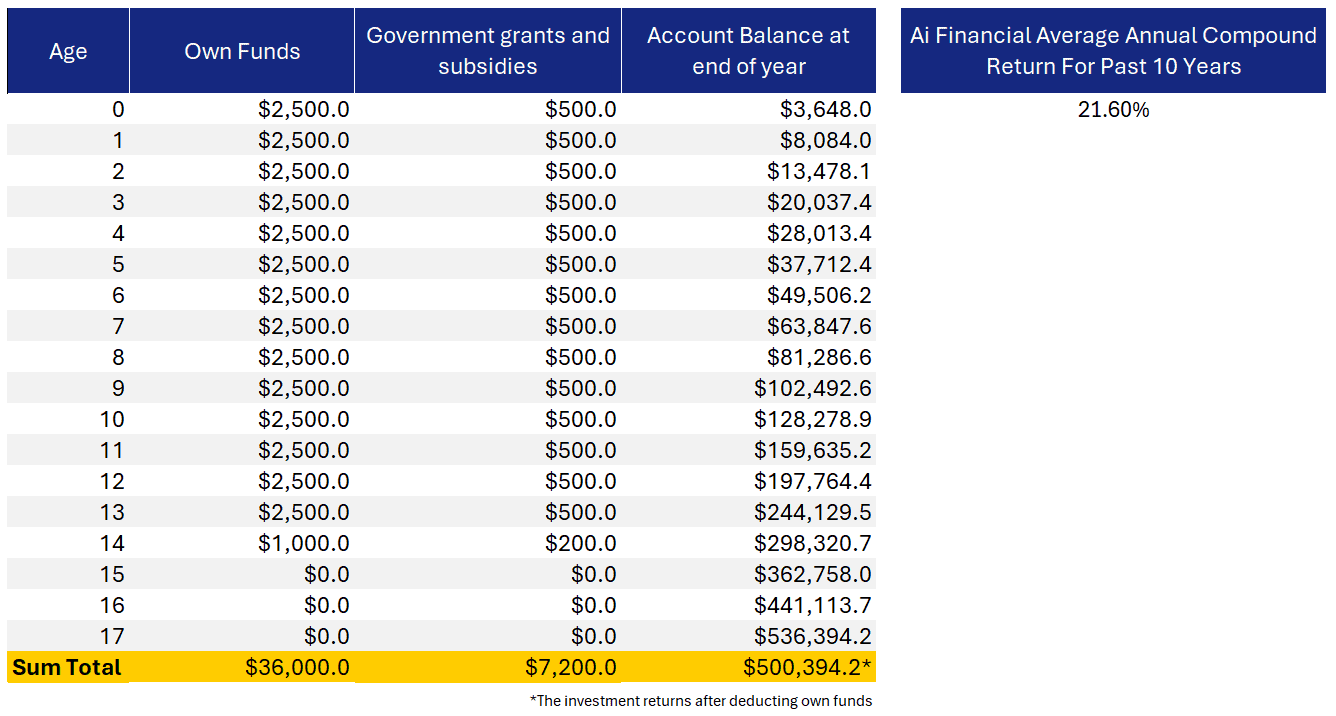

The lifetime contribution limit for each beneficiary is CAD 50,000.

Let’s simulate how much financial support your child could potentially receive from birth to adulthood based on our historical investment returns:

If you maintain annual deposits from the beneficiary‘s birth until they turn 14, you actually only need to save $1,000 in the 14th year to receive the government’s final $200 grant (since the maximum government support is $7,200). If the goal is merely to maximize the grant, we’ve already achieved that, and there’s no need to continue contributing. By the time the beneficiary turns 18 and heads to university, subtracting the actual contributions of $36,000, the account balance will be totals $500,000. For a newly adult child, this is a sum that can enable them to achieve financial freedom ahead of schedule.

Maybe you find the 21.6% return uncertain or not sufficiently reliable, using the annual average return rate of the SPY 500 (approximately 15%), the beneficiary would still receive around $210,000 in financial support.

Young adults is and will be facing greater pressures than imagined in modern society. Many of them struggle with challenges like affording a home, finding their desired job, and managing student loans or other debts. If you can provide substantial assistance to your child when they most need financial support, at a relatively small cost and without adding pressure to your own life, it would be the best coming-of-age gift you could give your loves.

FHSA - First Home Savings Account

The First Home Savings Account (FHSA) is a new registered plan introduced in Canada on April 1, 2023, following the success of the Tax-Free Savings Account (TFSA). The FHSA aims to help first-time homebuyers save for a home by combining the benefits of a TFSA and a Registered Retirement Savings Plan (RRSP). Contributions to an FHSA are tax-deductible, investment income grows tax-free, and withdrawals for purchasing a first home are also tax-free. This plan provides convenient and beneficial financial support for achieving homeownership.

To open an FHSA, you must:

- Be at least 18 years old and under 71 years old by December 31 of the current year.

- Be a Canadian resident.

- Not own property in Canada in the year of opening the account or in the previous four years, and have never used any property owned by you or your spouse as a primary residence.

The FHSA can be held for a maximum of 15 years. Accounts can be opened through any institution that offers TFSA and RRSP services, such as banks, credit unions, insurance companies, and trust companies.

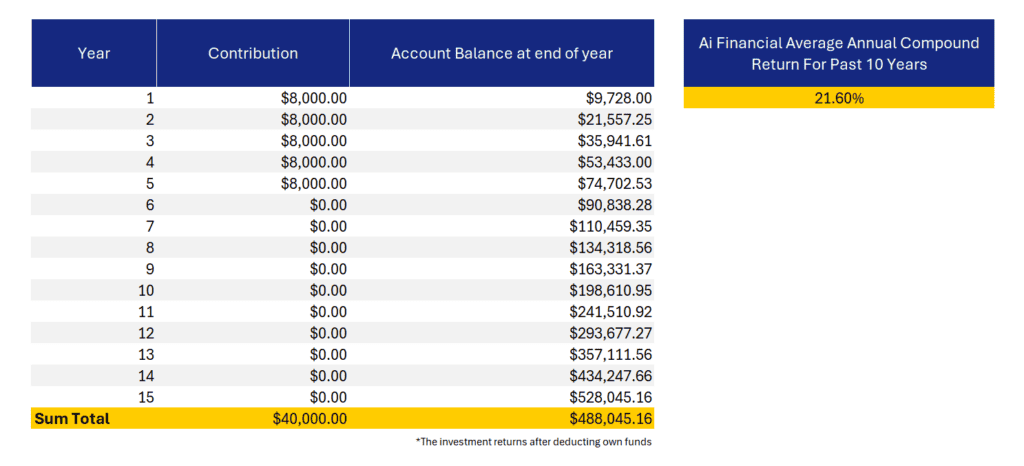

At Ai Financial, our historical investment returns have successfully doubled our clients’ assets within five years.

Let’s simulate how much financial support your could potentially receive within 15 years based on our historical investment returns:

If you max out your TFSA contribution limit every year, you have the opportunity to achieve tax-free investment gains of $480,000 after 15 years based on Ai Financial’s historical average annual return of 21.6% (excluding the initial $40,000 principal). This would provide substantial support for a down payment on a new home.

Maybe you’re concerned about our return rate accuracy, using the historical average annual return of the SPY 500 (approximately 15%), you could still achieve investment gains of $210,000 after 15 years. If you have a spouse, doubling your contribution room and returns can effectively help alleviate the pressure of buying a home.

Investment Products Overview - Segregated Funds

All the accounts can hold various investment products, such as stocks, bonds, mutual funds, and ETFs. Ai Financial recommends choosing Segregated Funds as an investment option. With our industry-leading investment insights and fund selection capabilities, we aim to provide clients with the potential for doubling their investment returns over five years at 20%+ return rate.

Segregated Funds are like Mutual Funds, as they are market-based investments. They pool substantial amounts of money managed by fund managers who invest in stocks, bonds, or other securities to enhance the overall value of the fund and generate returns for investors.

Benefits of Segregated Funds

Choose one of the guarantees for maturity and death benefits, 75% or 100% of the amount invested, to help ensure your savings remain protected. This means that when your investment reaches its maturity date or when you pass away, if your investment is worth less than its guaranteed value, the insurance protection will top you up. Naturally, it will be proportionally reduced by any withdrawals.

If you think you might want to pass along your assets to your loved ones, segregated funds offer a great solution.

Segregated funds help you preserve your money by:

- Guaranteeing that your beneficiaries receive a certain percentage of your investments

- Allowing your proceeds to pass directly to your beneficiaries without going through probate (the process by which a court formally approves a Will). This means:

- Your loved ones receive the money faster

- Your estate remains private

- More money is passed along

This means that creditors may not be able to take the funds you have in your segregated fund contract.

While management fees for Segregated Funds may be slightly higher than those for Mutual Funds, the additional protection and convenience often justify the costs, potentially saving investors from significant expenses later.

Mutual Funds

- Simple and easy to buy and sell

- Manage by professional team

- Diversification

- Low cost and high transparency

- Strong liquidity, providing cash flow

- Tax convenience

- Accept PAD

- Principal guarantee

- Probate-free

- Named beneficiary

- Creditor protection

Segregated Funds

- Simple and easy to buy and sell

- Manage by professional team

- Diversification

- Low cost and high transparency

- Strong liquidity, providing cash flow

- Tax convenience

- Accept PAD

- Principal guarantee

- Probate-free

- Named beneficiary

- Creditor protection

Investing in public funds inherently diversifies your portfolio. By selecting leading companies in top sectors, our fund combinations include dozens or even hundreds of businesses, providing sufficient diversification. Therefore, investors don’t need to spread their funds further, as this could lead to poor returns or losses.

While Segregated Funds may have slightly higher management fees, it’s essential to focus on the quality of the investment and long-term returns rather than just costs. Cheap options aren’t always the best; investing requires careful consideration.

Lastly, it’s important to note that Segregated Funds are not primarily for wealth transfer; they are genuine investment products that provide numerous features, allowing for long-term investment.

You may also interested in

What is an investment loan?

Can this loan last a lifetime? Interest-only payments? Tax-deductible? Is it a private loan? Is the threshold high?

Invest with TFSA

A Tax-Free Savings Account (TFSA) provides you with a flexible way to save for a financial goal, while growing your money tax-free……

Invest in RRSP-Invest wisely, retire early

According to a recent survey by BMO, due to inflation and rising prices, Canadians now believe they need 1.7 million dollars in savings to retire……

Why do you need segregated funds for retirement?

Segregated funds are a popular choice for group savings and retirement plans. They provide access to high-end and unique……