Understanding the RRSP - Are You Throwing Money Away?

A Registered Retirement Savings Plan can help you save for retirement. Before March tax filing time, there is often a rush to buy RRSPs. That’s because RRSPs can offer tax advantages. And the earlier you start saving for your retirement, the better. A longer time horizon and compound interest make investing early for your retirement a good idea. Learn more about RRSPs and how they work.

What’s in this article?

Basic points about RRSP:

- An RRSP account needs to be opened.

- The account can be purchased by the individual, their spouse, or common-law partner.

- Money contributed to an RRSP can reduce taxable income, potentially lowering your tax bracket.

- However, withdrawals from an RRSP may be subject to taxation.

RRSP types and features

Individual RRSP

Individual RRSP is the most common RRSP type and the one most likely to be used by salaried individuals. When purchasing, it is essential to consider the contribution limit; otherwise, exceeding this limit will result in a 1% penalty per month to the government.

As a government-registered account with the CRA, the RRSP has a contribution limit. The formula for calculating this limit is:

RRSP Contribution Room for the Year = Previous Year’s Earned Income x 18%

This means that when filing taxes, the earned income reported to the CRA from the previous year is multiplied by 18% to determine the RRSP contribution room for the current year. Any income not reported to the CRA is not considered in the earned income calculation.

For example:

If Ben reported an income of $100,000 in 2022, his RRSP contribution room for 2023 would be: $100,000 x 18% = $18,000.

Thus, Ben’s RRSP contribution room increases by $18,000 in 2023.

However, this contribution room is not unlimited. The government sets annual contribution limits for RRSPs. The table below shows the RRSP limits for 2021 to 2023, with the maximum limit for 2024 being $31,560. For instance, if your earned income is $200,000, the formula would calculate a contribution room of $36,000, but the government caps the allowable RRSP contribution at $31,560. Exceeding this limit is not permitted.

In conclude: The maximum contribution you can make to your RRSP is 18% of your previous year’s income or the current fixed contribution limit.

| Year | Limit |

|---|---|

|

2018 |

$ 26,230 |

|

2019 |

$ 26,500 |

|

2020 |

$ 27,230 |

|

2021 |

$ 27,830 |

|

2022 |

$ 29,210 |

|

2023 |

$ 30,780 |

|

2024 |

$ 31,560 |

The RRSP limit can be accumulated, meaning if you didn’t use your contribution room in previous years, you can carry it forward and use it in future years. Contributions can be made monthly, annually, or at any time as long as you have available contribution room.

The contribution limit can be checked through various methods:

- CRA Website: Log in to your CRA My Account and follow the prompts to check your RRSP contribution limit.

- Notice of Assessment (NOA): Received after filing taxes, this document clearly states your RRSP contribution limit, how much you’ve used, and the remaining RRSP room.

- Call CRA: Dial 1-800-959-8281 for a voice service. Have your last year’s tax information ready and follow the prompts to check your RRSP limit.

- Consult Your Accountant: If you use an accountant for tax filing, they can provide information on your RRSP contribution limit.

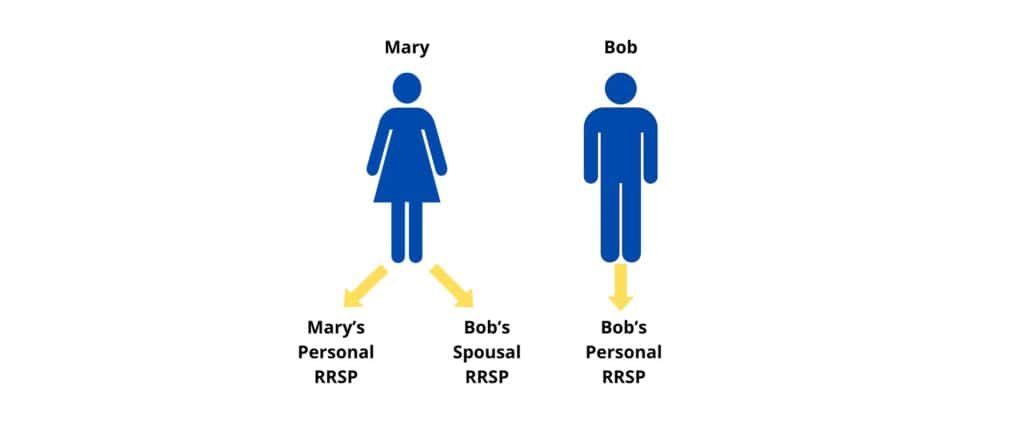

Spousal RRSP

Spousal RRSP is particularly beneficial for couples with significant income disparity, aimed at reducing the total tax payable by the couple.

This type of RRSP is suitable when there is a notable income gap between spouses. For instance, if the husband earns $150,000 annually and the wife earns $40,000, the husband can use his RRSP contribution room to contribute to an RRSP for the wife, known as a Spousal RRSP.

There is a restriction with Spousal RRSPs: withdrawals made within 3 years are attributed to the contributor (usually the husband) for tax purposes. After 3 years, withdrawals are taxed as income for the spouse (typically the wife).

Many people find it confusing to understand the roles within a Spousal RRSP, as illustrated in the diagram.

- Contributor: The contributor is the individual who provides the RRSP contribution room, in this case, the higher-earning husband (Bob).

- Owner: The owner is the individual who owns the RRSP, in this case, the wife (Mary).

Because this RRSP is in Mary’s name, Bob, as the contributor, does not have control over this RRSP and cannot participate in activities related to this account.

Group RRSP

A Group RRSP is typically a retirement benefit provided by companies to their employees. In Canada, large national institutions such as government, healthcare, teachers’ unions, and some large banks offer this type of benefit. So, what are the advantages and disadvantages of a Group RRSP?

Advantages:

- Employer Matching: If you participate in your company’s Group RRSP, the company will match a portion of your contributions. However, this still counts towards your own RRSP contribution limit.

- Contribution Limits: The company sets a matching limit. For example, some companies match contributions dollar-for-dollar (1:1), meaning if you contribute 4%, the company will also contribute 4%. Others may have a lower match, such as 1:0.5, where if you contribute 4%, the company contributes 2%. This varies by company but is always a benefit to the employee.

Disadvantages:

- Limited Investment Options: Group RRSPs often have limited investment choices, with low personal involvement. Employees usually complete a questionnaire to determine their risk tolerance (conservative, aggressive, etc.), and the plan managers make investment choices based on the results. Few companies allow employees to choose their own investments.

- Locked-in Funds: While employed at the company, you cannot transfer your Group RRSP out; it is locked in. This type of account is also known as a Locked-In RRSP (LIRA). Only upon leaving the company can you transfer it out, and even then, it must go into another locked RRSP account.

All three types of RRSPs discussed here (individual, spousal, and group) use your own RRSP contribution room. Whether you buy it yourself, through your company, or for your spouse, it all comes out of your personal RRSP limit. Exceeding this limit will result in a penalty of 1% per month on the excess amount.

Misconception

Besides the types of RRSP purchases, some people have misconceptions when considering buying RRSPs. Here are three common misconceptions explained:

Misconception 1: RRSPs are pointless and shouldn't be bought

This misconception stems from the belief that while RRSP contributions provide tax deductions now, withdrawals in the future are still taxable, making RRSPs seemingly ineffective.

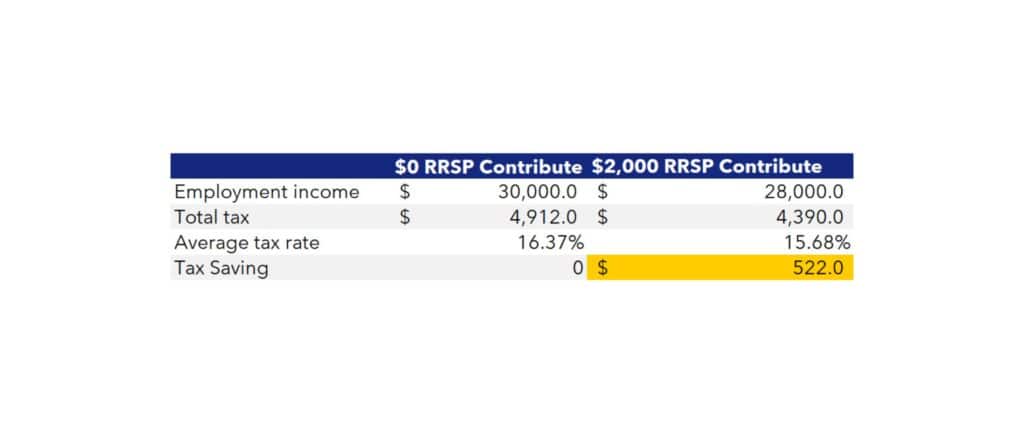

This viewpoint is incorrect because RRSPs offer not only tax deductions but also a crucial tax deferral benefit. When you contribute to an RRSP while working, the contributed amount is deducted from your taxable income for that year. For instance, consider the following scenario:

If a salaried individual earns $30,000 in a year and does not contribute to RRSPs, they will owe $4,912 in taxes. However, by contributing $2,000 to an RRSP, their taxable income reduces to $28,000, resulting in taxes of $4,390, save $522 on tax.

Moreover, when this $2,000 is withdrawn during retirement when the individual has no other income, it would be taxed at a much lower rate or possibly not taxed at all, thanks to the basic personal tax exemption each year (which is over $10,000 currently). Therefore, the $522 tax refund effectively becomes additional savings. This illustrates the dual benefits of tax deduction and tax deferral provided by RRSPs.

Misconception 2: RRSPs can only be purchased during RRSP season

This misconception arises from a misunderstanding of RRSP purchasing rules.

RRSP contributions can be made at any time during the year. Contributions made outside the “RRSP season” still qualify for reducing the taxable income for that year. Contributions made by March 1st of the following year can also be applied to the previous year’s RRSP contribution limit, thereby reducing taxes paid for that year. For example, March 1, 2023, is the deadline for contributing to the RRSP limit for the tax year 2022. The period from early in the year until this deadline is commonly known as RRSP Season.

During RRSP Season, many financial institutions offer RRSP loans to assist individuals who need to make contributions. These loans may offer different advantages depending on the institution, and interested parties are encouraged to contact us for more information.

Misconception 3: RRSP funds cannot be withdrawn before retirement

Similarly, this misconception stems from unfamiliarity with RRSP rules and may deter people from investing in RRSPs.

In fact, funds deposited into an RRSP can be withdrawn at any time. However, if withdrawn before retirement, the amount is considered as income for that year and subject to withholding tax, which varies based on the province and the amount withdrawn. Funds withdrawn after retirement do not incur withholding tax.

Moreover, the government provides beneficial options where RRSP withdrawals under certain circumstances (like the Home Buyers’ Plan or Lifelong Learning Plan) do not count as taxable income, provided the withdrawn amount is repaid within specified timelines.

RRSP investing strategy

Understanding the types of RRSPs and their misconceptions, the next step is where to open an account and purchase RRSPs. After buying them, how should they be managed? This raises the question of RRSP investment strategy.

Apart from Canada’s major banks (RBC, TD, BMO, CIBC, and Scotia Bank), many different financial institutions in Canada, such as insurance companies, mutual fund companies, and trust companies, can also open RRSP accounts and facilitate RRSP purchases. As long as your total contributions do not exceed the registered limit with the CRA, you have flexibility in where you can open an RRSP account.

After opening an RRSP account and purchasing RRSPs through these financial institutions, another crucial consideration is how to manage them. In summary, there are three main approaches:

First, in general, RRSP account holders often opt to open savings accounts to place their RRSP funds, aiming to earn some interest. For those seeking a slightly better option, they might open a GIC (Guaranteed Investment Certificate) or a HISA (High-Interest Savings Account) to safeguard these retirement funds from losses.

However, these savings accounts, while appearing to accrue interest annually, actually guarantee a loss. This is because the interest earned typically cannot outpace inflation. While it may protect the nominal value of the funds, the real purchasing power diminishes over time.

For example:Suppose $100,000 is placed in a savings account. After 10 or 20 years until retirement, despite earning some interest annually (e.g., around 4%), this interest rate would not keep pace with inflation, which is currently around 6.8%. Even in years with lower inflation rates (e.g., 2-3%), the interest earned may only be 1-2%, significantly less than the rate of currency depreciation. Thus, year after year, by the time the funds are withdrawn, they may no longer be sufficient to support a lengthy retirement.

Second, for those who choose not to keep their RRSP in these savings accounts, they may consider investing in the stock market. However, without being a professional investor, this option carries higher risks. Placing money in one or a few stocks exposes the RRSP to significant losses if those stocks perform poorly. Additionally, trading stocks within the stock market is akin to making withdrawals from the RRSP, impacting the tax and income aspects for the RRSP holder.

The third and final option is to invest RRSP funds in mutual funds purchased through banks or segregated funds purchased through insurance companies. This is a strategy worth serious consideration.

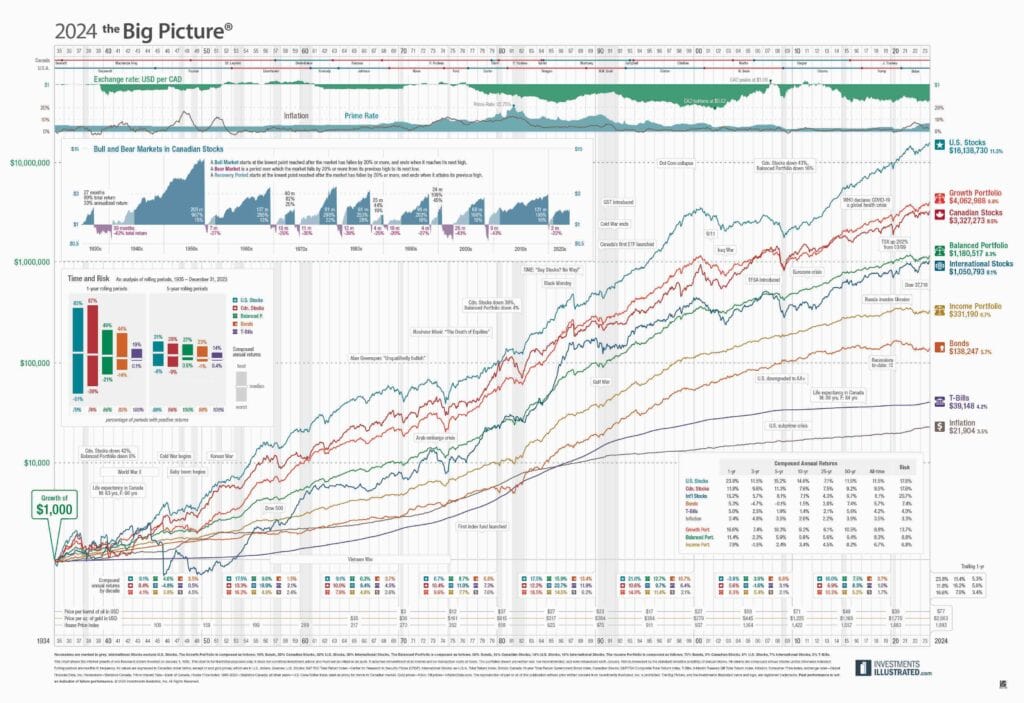

The reason is straightforward; here’s the big picture.

It shows the long-term trends of the market. From this graph, you can see:

If a person invested $1,000 in the U.S. market in 1934 (the top line on the graph), by the end of 2021, their assets would have grown to $14,861,397, a multiplier of 14,861. If invested in the Canadian market, it would have grown to $3,162,135, a multiplier of 3,162. This represents the performance in the North American markets.

Following this trend, if someone were to invest their RRSP funds in a similar manner now, and adhering to the characteristics of RRSPs for retirement planning over 20 years, the trend from this graph shows that substantial profit accumulation can be achieved with the right investment targets and consistent long-term holding.

In other words, investing RRSP funds according to market trends inevitably leads to profit. This is primarily what RRSPs are intended for—retirement planning. If someone had invested their RRSP funds in this market 20 years ago, it would already be a considerable sum today.

Of course, this process is not easy to manage independently, and it’s best to entrust management to professionals. Individuals should follow certain disciplines or principles:

- Invest in funds.

- Commit to long-term investments.

- Engage in long-term, protected, and correct fund investments.

In conclusion, effectively utilizing Canada’s government-provided RRSP benefits not only helps secure a comfortable retirement but also aids in reducing the burden on Canada’s pension system.

What to do next?

If your RRSP funds are currently idle, you can schedule a consultation with a segregated fund agent at Ai Financial to discuss how to make the most of these funds and plan for your future retirement.

You may also interested in

What is an investment loan?

Can this loan last a lifetime? Interest-only payments? Tax-deductible? Is it a private loan? Is the threshold high?

Mutual/Segregated Funds Vs. Stocks

If you’re new to investing, it’s crucial to understand the differences between mutual/segregated funds and stocks to determine the best……

Invest in RRSP-Invest wisely, retire early

According to a recent survey by BMO, due to inflation and rising prices, Canadians now believe they need 1.7 million dollars in savings to retire……