If you’re thinking about building wealth for your family, you may be considering mutual funds. However, segregated funds are another avenue worth considering. While both offer potential for growth, segregated funds provide unique estate planning advantages that mutual funds simply can’t match, be it avoiding probate fees, minimizing taxes, or simply the efficiency of passing on your inheritance. Additionally, traditional methods of passing on wealth—like through a will—can sometimes be a slow, costly process due to probate and the associated taxes and fees.

In this article, we’ll explore how segregated funds can help you avoid these issues by bypassing probate, minimizing taxes, and ensuring that your beneficiaries receive their inheritance faster and more efficiently than with other investment options, such as mutual funds.

How Segregated Funds Bypass Probate (And Why That Matters)

One of the standout features of segregated funds is that they bypass the probate process altogether. But what does that mean, and why is it such a big deal in estate planning?

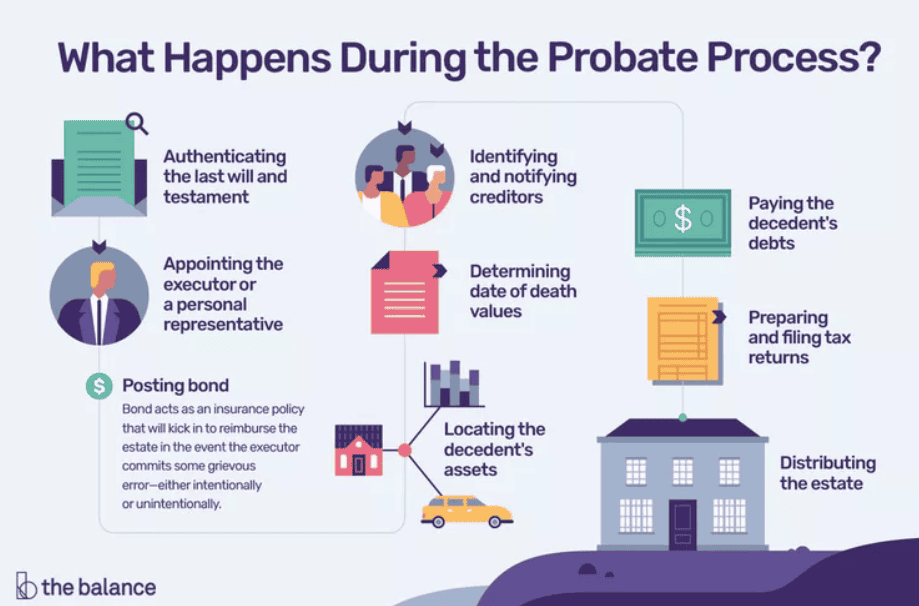

What is Probate?

Probate is the legal process that occurs after someone passes away. It involves validating the deceased person’s will, paying off any outstanding debts, and distributing the assets according to the will or the laws of the jurisdiction if there’s no will. This process, although necessary, can be time-consuming and costly, often taking several months and incurring legal and administrative fees that can eat into the estate’s value. In some provinces, probate fees can be as high as 5% of the estate’s value!

Benefit of segregated funds

Here’s where segregated funds shine: If you’ve named a beneficiary on your segregated fund, the fund is paid directly to that beneficiary upon your death, outside of probate. This means your heirs can receive their inheritance quickly, without having to wait for the probate process to unfold.

For example, let’s say you have a segregated fund worth $500,000 and you’ve designated your daughter as the beneficiary. When you pass away, the $500,000 will go straight to her, bypassing probate altogether, and avoiding any associated fees or delays.

Segregated funds therefore allow you to control who gets the money and when, with no need for court intervention.

The Process for Mutual Funds: More Steps, More Fees

Now, let’s talk about mutual funds. While they can be a solid investment, the transfer of mutual fund assets upon your death is a different, more complicated process.

When someone passes away and owns mutual funds, the process typically works like this:

- The Mutual Fund Becomes Part of the Estate:

Unlike segregated funds, mutual funds are usually not directly transferred to beneficiaries unless a transfer-on-death (TOD) designation has been made (which isn’t available for all mutual funds). Instead, the mutual fund becomes part of the deceased’s estate. - Probate Proceedings Begin:

The mutual fund holdings are now part of the probate process. The executor of your estate will need to go through the formalities of probating the will, which, as mentioned, can take time and involve various legal fees. In addition to court and administrative costs, the estate might also have to pay taxes, which can further reduce the overall value of the inheritance.