You can transfer the RESP account to another sibling of the beneficiary.

If the subscriber or their spouse has available contribution room in their RRSP (Registered Retirement Savings Plan), funds can be transferred into the RRSP.

Take your time before withdrawing funds from the account while it’s still valid. You can retain them temporarily to prevent any future needs. Typically, RESP accounts have a lifespan of 35 years.

If you wish to withdraw, you’ll need to return the government grant portion to the government, and earnings will be subject to taxation plus a 20% penalty. Some RESP investment plans/types might have additional restrictions; it’s advisable to inquire about these when opening the account.

The government grants associated with an RESP investment account mainly consist of two types:

CESG, which stands for Canada Education Savings Grant, requires contributions to be eligible.

This grant is directly contributed by the government into the account and grows tax-free. The CESG matches contributions by 20% annually, up to a maximum of $500 per year. By investing $2,500 annually in an RESP, you can receive the maximum $500 government grant. The lifetime limit for CESG is $7,200.

Requirements for application:

- The beneficiary must be a Canadian resident.

- To open an RESP account, you need a Social Insurance Number (SIN).

- If the age is between 16-17 years old, there must be at least $2,000 in contributions made to the RESP account before the beneficiary turns 16, and these funds should not have been withdrawn.

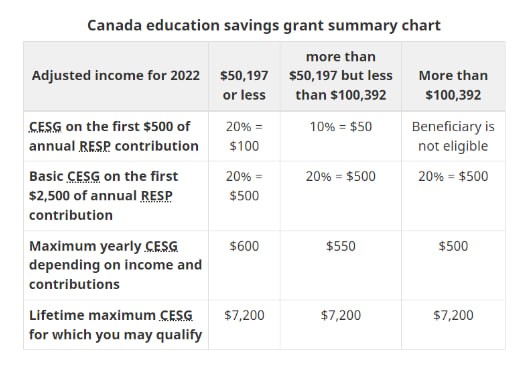

ACESG, short for Additional Canada Education Savings Grant, is available for families with incomes below a certain threshold. The government provides an extra 10% to 20% matching grant on the first $500 contributed annually, amounting to approximately $50 to $100. Below is the 2022 guideline:

CLB, which stands for Canada Learning Bond, is available without the need for contributions. It is an additional government grant provided to low-income families.

Compared to CESG, CLB doesn’t require contributions. Families eligible for CLB can receive government funds by simply opening the account, even without any deposits. Upon the first account opening, families meeting the CLB eligibility criteria can receive $500. Additionally, they can get an extra $100 annually until the child turns 15. Similar to CESG, the investment returns for CLB also grow tax-free, with a lifetime limit of $2,000.

It’s advisable to open an RESP education fund account for your child as early as possible because eligibility for CLB is based on family income. If you wait until your income increases before opening an RESP investment account, you might miss out on CLB eligibility.

What is an investment loan?

Can this loan last a lifetime? Interest-only payments? Tax-deductible? Is it a private loan? Is the threshold high?