What is CPP and why we DON’T like it

The Canada Pension Plan (CPP) is a government-led retirement program that was launched in 1965 to help add a little more shine to your golden years. It was originally meant to provide you with 25% of your pre-retirement income, but thanks to something called the CPP Enhancement, which started being phased in during 2019, you can now contribute more to your CPP in order to have a larger pension — up to 33% of your pre-retirement income.

If you’ve made more than $3,500 a year (except if you live in Québec, which has its own Québec Pension Plan (QPP)), you’ve already paid into the CPP, and so has your employer, at the government-mandated 50% share. The good news is that once you hit 60, you can start collecting your pension payments. Depending on your financial situation, however, you may not want to take your CPP payments right away because for every year you wait, your CPP payout increases. As for how much your CPP payment will be, that depends on two main factors: how much you earned during your career and how old you are when you begin taking your pension. You reach the maximum amount when you hit 70, so if you can afford to hold off that long, it’s often best to wait. Here, we’ll explain the benefits and downsides to the different CPP timing options.

Who pays into the CPP?

In 2024, employees over the age of 18 who earn more than $3,500 per year must pay into the CPP. (As we mentioned above, if you live in Québec, you’ll pay into the QPP, which has a slightly higher rate.) CPP contributions are split equally between employer and employee, based on the employee’s income up to a maximum set by the federal government. If you make more than $68,500 in 2024, you’ll contribute the maximum amount to the CPP.

What is the max CPP contribution in 2023?

To receive the maximum CPP payment, you need to have made the max CPP contribution each year for at least 39 years. The maximum employee contribution changes each year. In 2024, it is $3,867.50, or 5.95% of your salary (less a $3,500 exemption), whichever is more. For self-employed people — who pay both the employer and employee contributions — the maximum CPP contribution is $7,735.

Pros and Cons of Deferring CPP

Starting at Age 60:

- Permanent reduction of up to 36% (0.6% per month before 65th birthday).

Starting at Age 70:

- Permanent increase of up to 42% (0.7% per month after 65th birthday).

Pros of Deferring to Age 70:

- Government Bears Risk: Investment and inflation risks are handled by the government.

- Inflation-Indexed: Payments increase with inflation.

- Longevity Protection: Higher payments provide more financial security in old age.

- Better Returns: Higher implied rate of return.

Cons:

- You need to use more of your savings while waiting.

- If you have poor health or need the money sooner, starting early might be better.

Is CPP taxed as income?

Yes, CPP is considered income and is fully taxable at your marginal tax rate. To avoid a big tax shock at the end of the year, you can request that income tax be deducted from each payment.

Can I share my CPP with my partner?

Yes, the CPP payments you receive can be shared with a lower-income spouse or partner. They can also be split in the case of separation or divorce. If one partner was out of the workforce, or worked part time to take care of a baby or child, there is a provision for child rearing that will exclude the lower-earning years from the CPP payment calculation, effectively increasing the CPP payment you can receive.

What are the average and maximum CPP monthly payments?

In 2024, the maximum CPP payout is $1,364.60 per month for new beneficiaries who start receiving CPP at 65. Although the max CPP payout is substantial, not everyone gets it. The average CPP in October 2023 was a much lower $758.32 per month. This is because not all people have contributed enough over their lifetimes to receive the full CPP payment, or because of scenarios such as survivor or disability benefits.

As we mentioned before, to receive the maximum CPP, you would have to be making the maximum CPP contribution for 39 years. The federal government sets the Year’s Maximum Pensionable Earnings (YMPE) every year. That number is the basis for both CPP and pension contributions. In 2023, the YMPE is $68,500. Here’s a helpful chart:

| Type of pension or benefit | Average monthly amount for new beneficiaries (2024) | Yearly average amount | Monthly maximum amount (2024) | Yearly maximum amount (2024) |

|---|---|---|---|---|

|

Retirement pension, age 65 |

$758.32 |

$9,099.84 |

$1,364.60 |

$16,375.30 |

|

Retirement pension, delayed to age 70 |

$1,079 |

$12,948 |

$1,937.73 |

$23,252.93 |

Is CPP Alone Enough for Retirement?

Understanding CPP and OAS Payments

Based on the most recent figures, if you’re over 75 and receiving the average CPP payment for 2023 ($760.07), that’s $9,120.84 annually. Adding the maximum OAS payment ($756.32), you get $1,516.39 per month, or $18,196.68 per year before taxes. This is often insufficient for most Canadians to comfortably retire. You may qualify for GIS if these are your only income sources.

Financial Planning for Retirement

Living simply and having your house paid off might allow you to get by on CPP and OAS alone, but having a backup plan is advisable. Consider setting up a Tax-Free Savings Account (TFSA) or a Registered Retirement Savings Plan (RRSP), or even both. You can estimate your retirement needs using our free retirement calculator, which also indicates if you’re saving enough or need to save more.

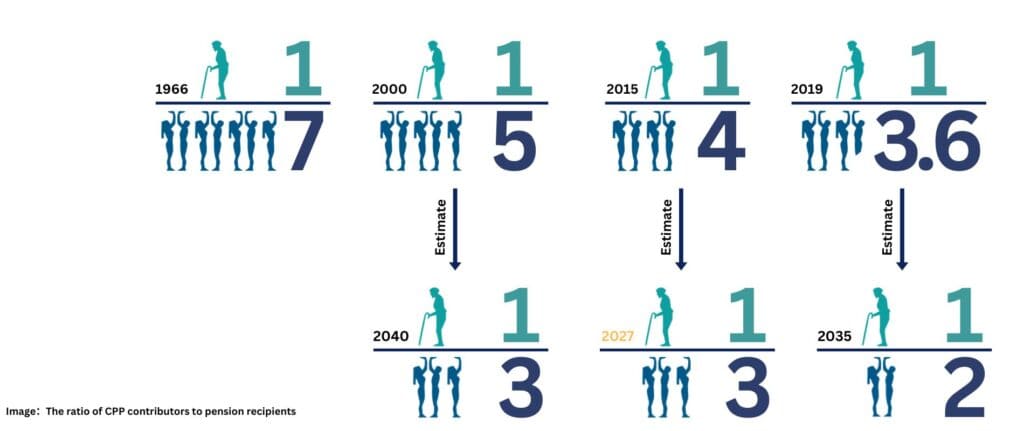

Historical CPP Contributions vs. Pension Recipients

- 1966: When the CPP was established, the ratio 7.7 working-age individuals for every senior

- 2000: The ratio was 5 working-age individuals for every senior, with a projection of 3:1 by 2040.

- 2015: The ratio was 4 working-age individuals for every senior, reaching the 3:1 by 2027, 13 years earlier than previous estimation.

- 2019: The ratio was 3.6 working-age individuals for every senior, with a projection of 2:1 by 2035.

Currently, there are 3.4 working-age individuals for every senior (2022). This is expected to decrease to 2:1 by 2035, indicating an accelerating trend.

Longevity and Quality of Retirement

Advancements in medical care, wellness products, healthy diets, exercise, and cosmetic procedures have significantly increased human lifespan. With more elderly individuals aiming for a high-quality retirement, the pressure on the working population to support them increases. How can we ensure a comfortable retirement under these circumstances?

Measures to Address the Decline in Support Ratios

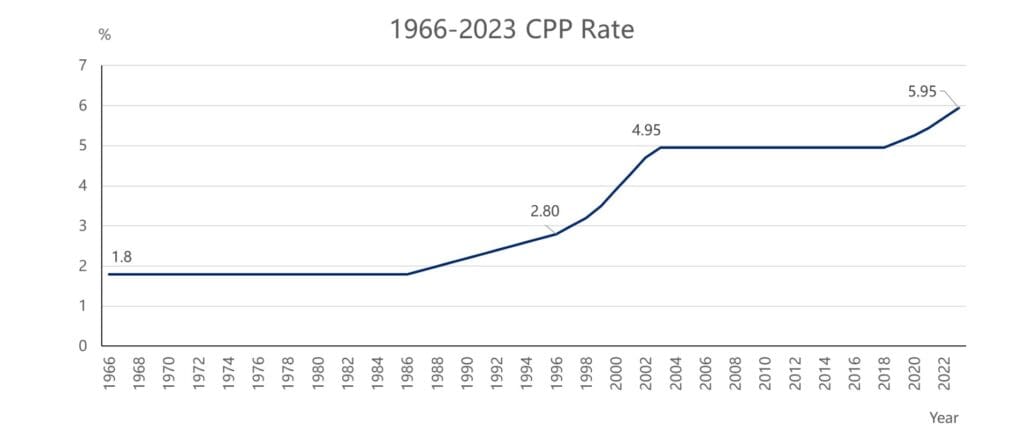

To slow the decline in the worker-to-retiree ratio, the government has implemented various measures, notably increasing the CPP contribution rate. The historical trends of CPP rates from 1966 to 2023 are as follows:

- 1966-1986: CPP rate remained at 1.8%.

- Late 1980s: CPP crisis led to an annual increase of 0.1%.

- 1998: Worsening crisis prompted varying annual increases.

- 1999: Establishment of the CPP Investment Board (CPPIB) to manage investments.

- 1999-2003: Due to successful CPPIB investments, the rate stabilized at 4.95%.

- 2019: Rising concerns about CPPIB’s sustainability led to gradual increases again.

- 2023: The rate reached 5.95%, indicating that investment returns alone couldn’t solve the issue.

The Importance of Personal Retirement Planning

This trend highlights the growing strain on national pensions. If retirees don’t plan their finances well, the burden will fall on their children, who will face higher CPP contributions.

Purchasing an RRSP is a long-term strategy to ensure a comfortable retirement and support the government’s efforts. It also helps reduce the financial burden on our children.

You may also interested in

What is an investment loan?

Can this loan last a lifetime? Interest-only payments? Tax-deductible? Is it a private loan? Is the threshold high?

Invest with TFSA

A Tax-Free Savings Account (TFSA) provides you with a flexible way to save for a financial goal, while growing your money tax-free……

Invest in RRSP-Invest wisely, retire early

According to a recent survey by BMO, due to inflation and rising prices, Canadians now believe they need 1.7 million dollars in savings to retire……

Why do you need segregated funds for retirement?

Segregated funds are a popular choice for group savings and retirement plans. They provide access to high-end and unique……