Learn how a Canadian couple used an investment loan strategy...

Read MoreCanada: The Widening Wealth Gap

Today, we are not here to discuss complex economic theories or abstract macro trends. Instead, we focus on a reality happening around us—often unnoticed: the Canada wealth gap is widening at an unprecedented pace.

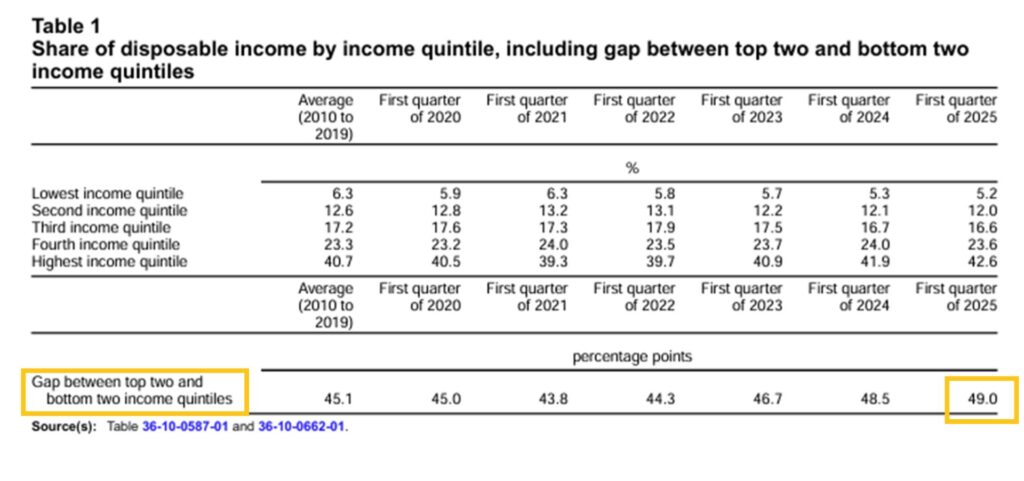

According to Statistics Canada, by Q1 2025 the wealthiest 40% of households controlled nearly 70% of the country’s disposable income, while the lowest 40% held only 18%. The gap of 49 percentage points is the largest since records began in 1999.

This is not distant news or political debate—it is what we see in our daily lives. Perhaps your neighbor just bought a new Tesla, while you are worrying about making your mortgage payment. You work hard, but bills and your savings account never seem to balance. The harder you try to catch up, the further behind you feel. This is not an illusion but a structural reality confirmed by data.

In the past decade, many believed that working, saving, and buying a home would lead to financial stability. The reality is different: wage growth lags far behind inflation, housing is no longer affordable for most, and wealth in capital markets has grown rapidly but concentrated in the hands of a few.

The consequence is serious: the middle class is disappearing. Hard-working individuals struggle to build wealth, while high-net-worth households grow stronger through investment income. Canada’s social structure is shifting from an “olive shape”—where the middle class dominates—to a pyramid, with more people at the bottom and wealth concentrated at the top.

This lecture will not stop at criticism or anxiety. Using data, analysis, and real cases, we aim to show the trajectory of this widening gap and highlight one possible solution: investment is the only way to break through.

At AiF, we believe investing is not reserved for the wealthy. It is the only realistic strategy for ordinary people to change their financial future. It is not a shortcut to instant riches, but it can mark a turning point in one’s financial strategy.

We will explore this topic in five parts:

- The Middle Class Is Sinking

- Savings Are Evaporating

- Assets Are Concentrating

- Generational Divide

- The AiF Investment Strategy

Part 1: The Middle Class Is Sinking

Let us begin with the first part: the middle class is sinking.

A chart from Statistics Canada, which has tracked disposable income distribution since 1999, reveals a troubling but clear trend: the gap between the wealthiest 40% and the poorest 40% has widened continuously over more than two decades. In the last five years, the pandemic and rising interest rates further fueled asset price growth—but that growth bypassed ordinary and middle-class households, accelerating the divide.

By Q1 2025, Statistics Canada reported that the wealthiest 40% held a share of disposable income 49 percentage points higher than the lowest 40%, the widest gap since 1999.

Does “hard work pays off” still hold?

For years, many believed that hard work guarantees reward. Yet the data clearly show otherwise: structural inequalities are pushing the middle class down.

We can picture income distribution as an elevator:

- The wealthy ride the upward “investment elevator,” gaining tens or hundreds of thousands in passive income each year.

- Ordinary workers ride a downward elevator, facing slow wage growth while carrying heavy mortgage and debt burdens.

This is not an individual failure but a systemic challenge.

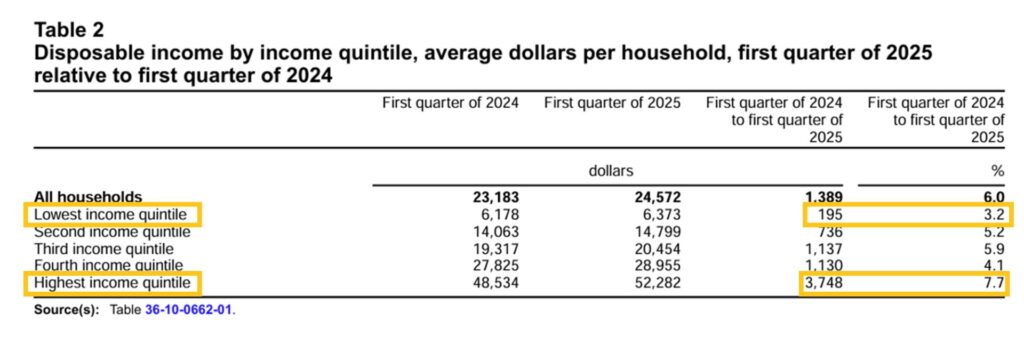

Income growth comparison

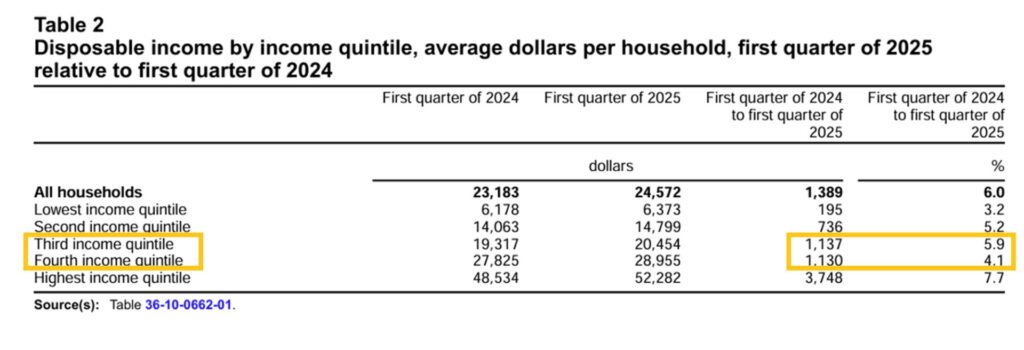

Comparing Q1 2024 to Q1 2025, disposable income growth rates across groups were:

- Low-income households: +3.2%

- Middle class (2nd to 4th quintiles): all below 6% (the average)

- High-income households: +7.7%

In short, only the wealthy outperformed the average. Low- and middle-income groups effectively became poorer in relative terms.

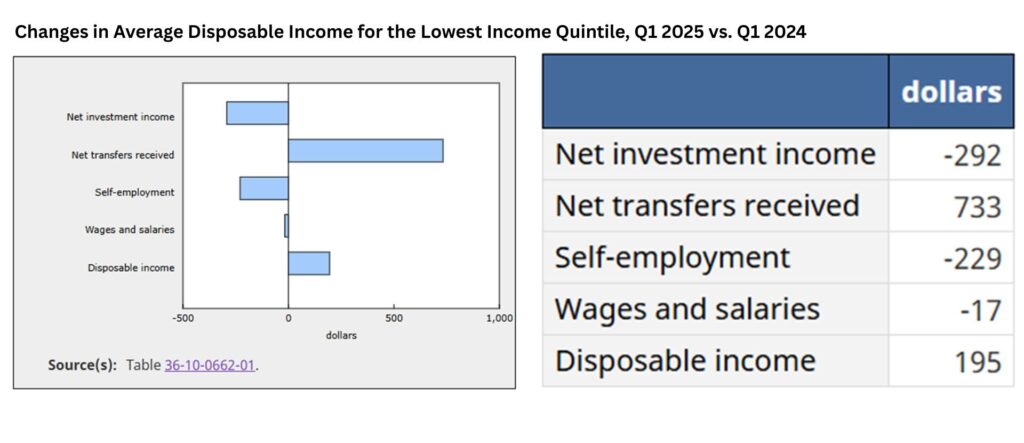

Why only 3.2% for low-income households?

Breaking down the lowest quintile:

- Transfers (e.g., government support or inheritance): +733

- Wages: +195

- Investment income: –292 (no real investment, some savings withdrawn)

- Self-employment income: –229

- Other wages: –17

The total growth of 3.2% came almost entirely from one-time transfers, offering little sustainability.

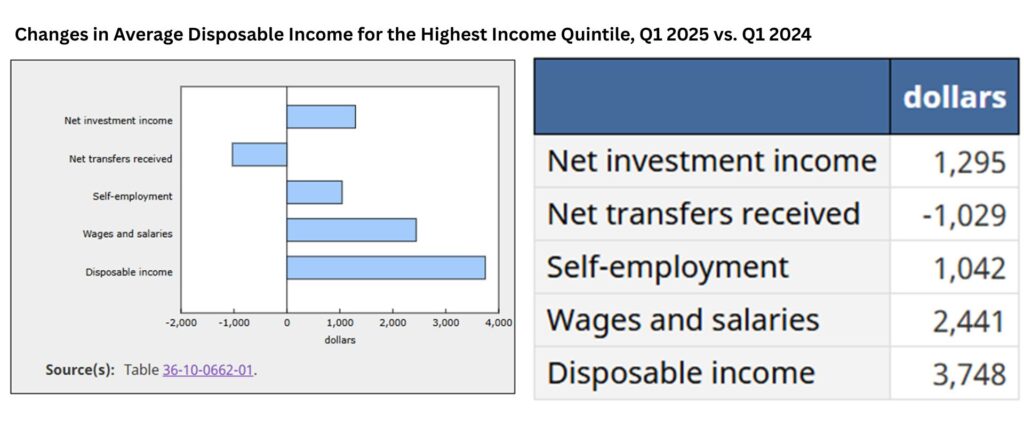

Why 7.7% for high-income households?

For the highest quintile:

- Investment income: +1295

- Self-employment income: +1042

- Wages: +2441

- Total disposable income: +3748

Even without transfers, they grew far above average by combining investments and higher earnings. Investment income was the true driver.

Wages are not the answer—investment is

This contrast proves that wage increases alone cannot close the gap. The primary driver for the wealthy is investment income—interest, dividends, capital gains, and net rental income.

Put simply: their money works for them.

The middle-class dilemma

Middle-class households, in contrast, face several challenges:

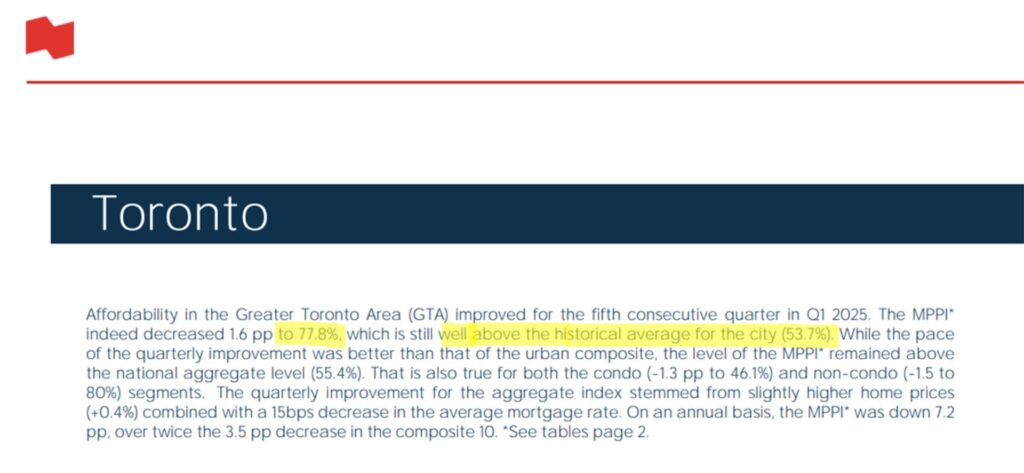

- Limited or negative investment income, offset by mortgage and credit card debt;

- Heavy housing costs, often 30–40% of monthly income;

- In Toronto, housing consumes up to 77.8% of pre-tax income; in Vancouver, homes cost 14 times median household income;

- Many misuse TFSAs as savings rather than investment accounts;

- Large shares of assets remain in bank deposits or GICs, missing out on compounding in equities and funds.

As a result, even diligent workers struggle to accumulate wealth, many falling into a “paycheck-to-paycheck” cycle.

The core of the wealth gap

Reports from RBC, TD, and others highlight the divide:

- High-income families hold over 50% of their assets in financial investments;

- Middle- and low-income families hold almost none.

This creates a massive net worth gap: the middle class sees income eaten away by debt servicing, while the wealthy enjoy steady passive cash flows.

Conclusion

The issue is not whether the middle class works hard, but whether they use the right financial tools and strategies. Leaving money idle in banks or GICs only ensures stagnation.

The reality is clear: wages cannot keep pace with inflation. Only through investment can households change their financial trajectory.

Part 2: Savings Are Evaporating

When you put your money in a GIC, your savings are effectively evaporating—because GIC growth can never keep pace with inflation.

Let’s look at the data to see who is saving and who is investing.

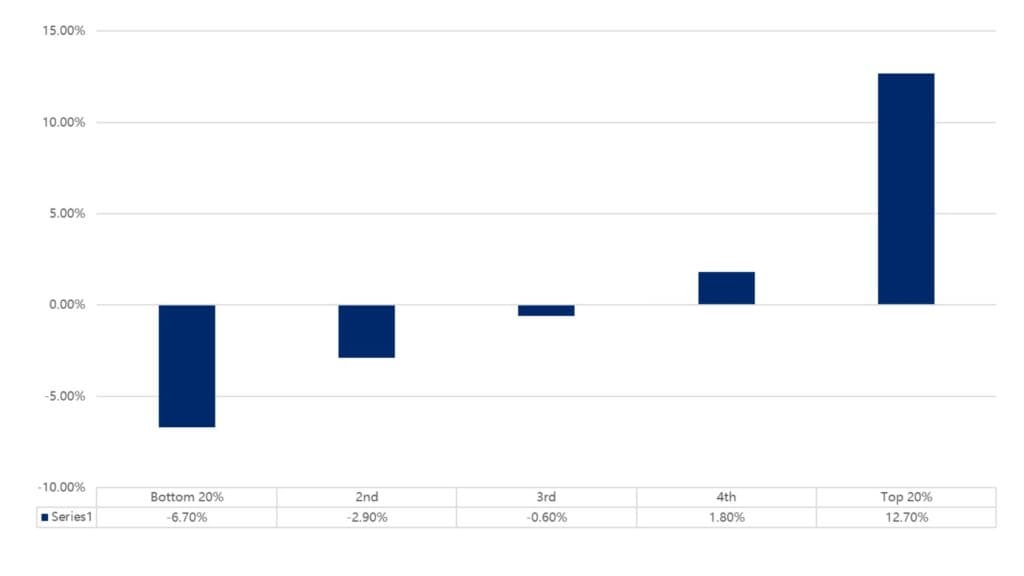

In Q1 2025, Canada’s average savings rates by income group showed a sharp contrast:

- Top 20% households: savings rate 12.7%.

This means they not only cover daily expenses but also have substantial funds to invest in financial markets or long-term assets, enabling continuous wealth growth. - Middle class (2nd, 3rd, and 4th quintiles):

- 2nd quintile: –2.9%

- 3rd quintile: –0.6%

- 4th quintile: 1.8% (barely positive, still below inflation)

In other words, most middle-class households have a savings rate near or below zero. They not only spend everything they earn but also rely on credit cards or loans to make ends meet.

- Bottom 20% households: savings rate –6.7%.

These families have no savings at all. Daily expenses are filled with borrowing, leading to rising debt levels and worsening financial stress.

The Middle-Class Dilemma

By Q1 2025, while national income rose overall, for the middle class the rise in living costs far outpaced wage growth. Housing, food, transportation, and energy costs all climbed. Interest rates have also surged in recent years, and even with slight recent cuts, borrowing costs remain far higher than pre-pandemic levels.

As a result, mortgage payments and credit card debt consumed most of middle-class disposable income. Statistics Canada data shows that median households had no savings left after paying mortgages and interest; many fell into negative savings.

Conclusion:

This chart reveals a striking fact: Canada’s savings and investment capacity is increasingly concentrated among the wealthiest households.

Most families, especially the middle class, are not lazy—they are simply trapped by high living costs and interest burdens, leaving them unable to invest. The data makes it clear: without investment, households become poorer over time.

Under inflation and high mortgage costs, middle- and low-income groups have little to no ability to accumulate wealth. Their savings are shrinking—or turning negative—while wealthy households expand their advantage through both savings and investment.

Part 3: Assets Are Concentrating

The reason you’re living paycheck to paycheck isn’t simply that you’re poor — it’s because you lack effective investment tools and strategies.

Many people don’t make use of vehicles like TFSA, RRSP, RESP, Non-Registered Accounts, or even Investment Loans. They haven’t established any clear plan for saving or allocating money into investments.

The real solution isn’t to work more overtime or pick up another side hustle to earn a little extra. The key is to let your money work for you — that’s the true meaning of investing.

Unlike the middle class, who are continually being pushed closer to poverty, assets are increasingly concentrating in the hands of the wealthy.

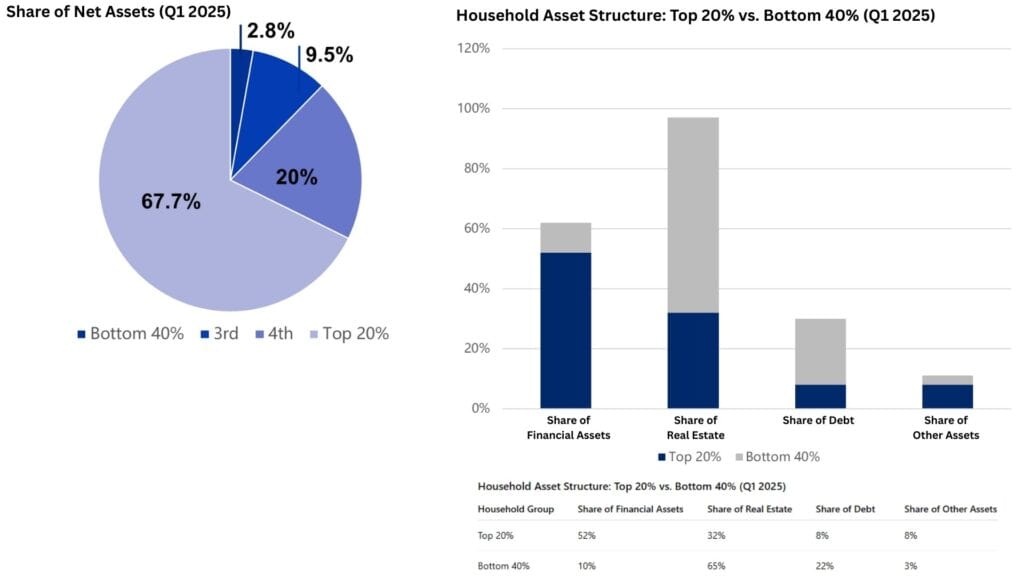

Wealth Concentration

This chart clearly reveals a shocking reality: in Canada, wealth is rapidly concentrating in the hands of a small minority.

According to the latest Household Economic Accounts data from Statistics Canada, in the first quarter of 2025:

- The wealthiest 20% of households controlled 67.7% of the nation’s net assets;

- The bottom 40% held only 2.8%;

- The middle class collectively accounted for 29.5%.

In other words, 20% of the population owns two-thirds of the wealth, while the remaining 80% share only one-third.

This directly reflects how mortgages, credit cards, and everyday expenses have almost completely drained the savings capacity of middle- and low-income families. That’s why today’s theme is “Canada: The Widening Wealth Gap.” The data for Q1 2025 has already hit a historic high. Wealth is becoming increasingly concentrated, and social polarization is getting worse.

Differences in Asset Structure

Let’s now look at how wealth is structured.

As wealth becomes more concentrated, high-income families and low-to-middle-income families have almost entirely different asset configurations.

- Top 20% (wealthy households):

The dark blue portion shows that their financial assets—stocks, mutual funds, corporate equity, pension plans, etc.—make up as much as 52%, generating ongoing investment income. - Bottom 40% (lower-income households):

Their main assets are concentrated in real estate (grey portion), and in most cases, this is simply their primary residence.

Many people consider a home a “necessity,” and while that sounds logical, for the bottom 40% of households, when their main source of wealth is their house, it usually comes with heavy mortgage debt. A primary residence is not truly an asset—it’s a liability.

Why? Because the mortgage drains their cash flow every month. Instead of generating income, it consumes it.

Whose House Is It Really?

For the wealthy, money works for them. For the poor, their house is merely collateral for the bank. The deed may say you’re the homeowner, but the interest payments all go to the bank. For lower-income families, your home is not really your asset—it belongs to the bank. You’re essentially working for the bank.

Many people believe their home will appreciate over time and lead to financial freedom. But the reality is: if your mortgage has already exhausted all your cash flow, that house is a negative asset.

Should You Sell?

Even if it’s your primary residence, if it leaves you with negative cash flow, you should seriously consider selling it. Renting may be better than being crushed under a mortgage. A house is meant to be lived in, not to drain your financial resources.

The same applies to investment properties. If an investment property generates negative cash flow, it’s not your wealth—it’s your burden.

Case Comparison

- High-Income Family (Family A):

Their assets are diversified—stocks, funds, pensions, corporate equity. Their house is just one part of their portfolio, with a relatively low loan-to-value ratio. Even if property prices fall, they still have stable cash flow. - Ordinary Middle-Class Family (Family B):

Most of their wealth is tied up in their home, purchased almost entirely with a mortgage. High monthly interest payments keep their cash flow negative. On paper, they “own” a home, but in reality, most of the equity belongs to the bank.

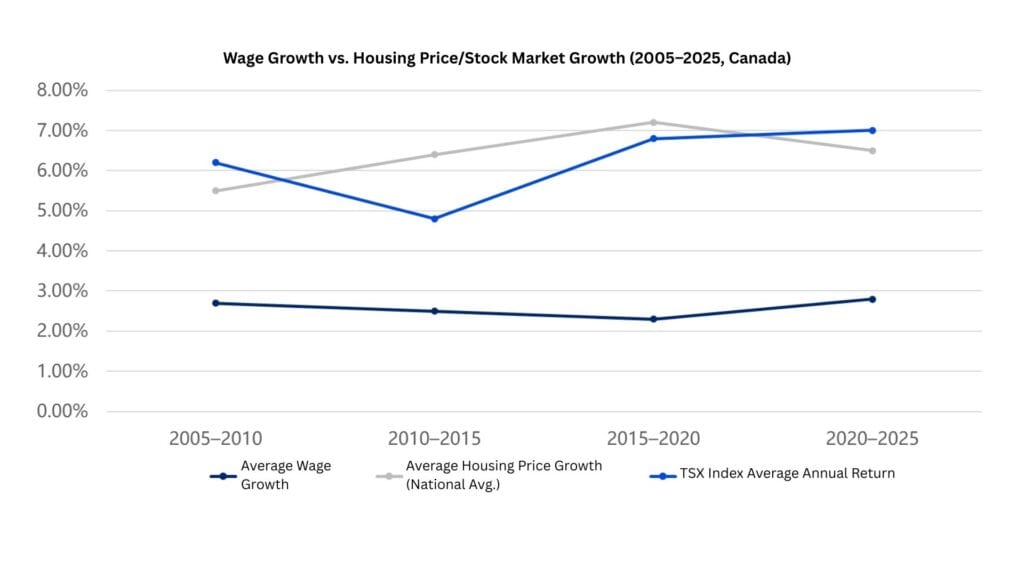

Wages vs. Housing Prices vs. Investment Returns

Many people ask: “If I just work harder and save more from my wages, can I keep up with wealth growth?”

The answer is no.

- Over the past 20 years, Canadian wages have only grown by 2%–3% annually;

- Housing prices have increased by 5.5%–6.5% annually;

- The Canadian stock market (TSX) has delivered average returns of 6.2%–7%;

- The U.S. stock market has performed even better, with average returns reaching 11.8%.

Housing prices have risen far faster than wages, and stock market returns have been double that of housing—and four times the growth of wages.

Summary

The wage curve has been almost flat, while the asset curve has risen sharply.

This is the core message of today’s lecture:

The fundamental driver of wealth inequality is not how hard you work, but whether you own investment assets.

Part 4: Generational Divide

As wealth continues to concentrate at the top, another phenomenon is unfolding: a growing generational divide.

Today’s young people are desperately trying to reduce their debt, fearing that loans will drag them down in the future. Meanwhile, households aged 55 and over are actively using leverage to expand their investments.

The financial logic between generations could not be more different.

Younger Generation: Passive Debt Repayment

Let’s start with those under 35.

Most of them are focused on paying down debt—working hard to repay student loans and credit card balances. By the time they reach 35, many are just getting married, and some are buying their first home, which means taking on a heavy mortgage.

That’s why housing prices in Canada today are so high that many young people simply cannot “get on the property ladder.” For them, debt is a burden, not a tool for wealth. As a result, the mindset of the younger generation is often: “pay off debt as quickly as possible” rather than “how can I use debt as leverage?”

Older Generation: Actively Leveraging

For households aged 55 and over, the picture is completely different.

They already own homes and assets, and they are more willing to make use of financial tools such as:

- Home equity loans

- Investment loans

They understand how to use debt as leverage to expand further into real estate and financial markets. Instead of passively repaying, they are actively using other people’s money to generate more wealth.

This creates a sharp contrast:

- Young people are passively burdened with debt, paying off loans but seeing little to no wealth growth;

- Older households are actively leveraging debt, using loans to generate investment returns and grow their wealth further.

Do Young People Really Have No Way Out?

Young people are not destined to remain trapped. Beyond mortgages, there is another form of leverage they can control—the investment loan.

The advantages of an investment loan are:

- It doesn’t depend on buying an expensive home first;

- You don’t need to afford a house upfront;

- With relatively small capital, you can unlock a much larger investment portfolio.

Unlike traditional “burden-style” debt, an investment loan is designed to generate cash flow.

In other words, young people are not unable to use leverage—they just need to learn how to use the right kind of leverage. What truly changes your wealth trajectory is not endlessly paying down debt, but putting your capital to work and letting it create new income.

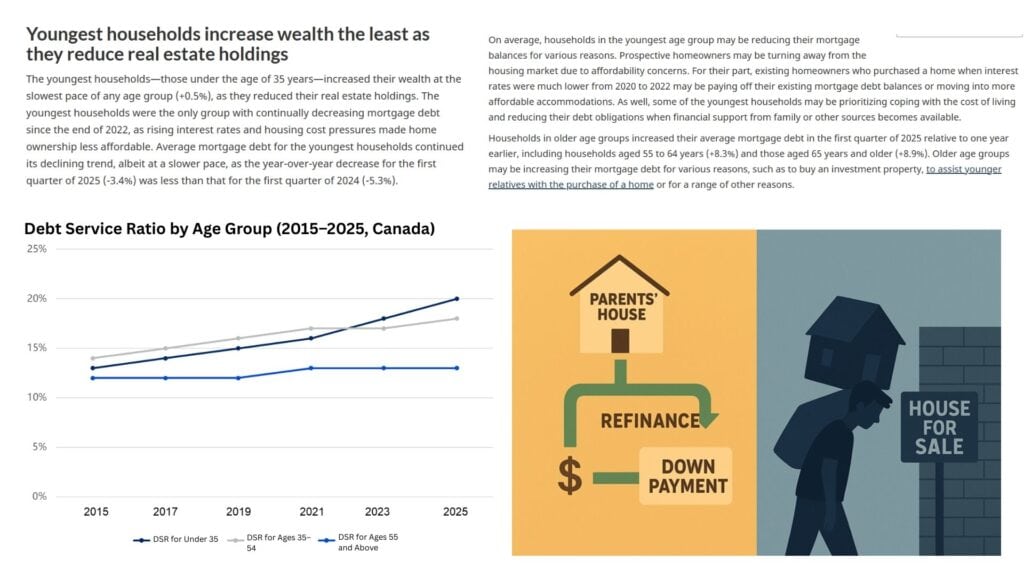

The Data Gap: Young People Pay More, Yet Struggle More

With rising interest rates, the debt pressure on young people has only grown. The data shows:

The dark blue line represents households under 35—their debt service ratio (DSR) has been steadily rising;

The light blue line represents households over 55—there is some increase, but much more modest.

This proves that the debt burden is significantly heavier for younger households.

The Financial Logic of “Relying on Parents”

This is why more and more young Canadians rely on their parents to buy homes.

This phenomenon, often referred to as “living off parents,” is not merely family support—it reflects a structural financial transfer of wealth.

Wealthier parents with assets often use home refinancing or investment loans to unlock leverage and release capital early, helping their children with down payments.

In other words, parents are not simply “handing out cash.” They are using financial tools to bring forward future cash flow and transfer it to the younger generation.

So, the logic behind “relying on parents” is this: the older generation sustains wealth growth through leverage, and transfers part of it to help the next generation enter the housing market.

Not Everyone Can “Rely on Parents”

But not every family has this option.

For young people without parental support, if they also don’t know how to use financial leverage, they may be completely shut out of both the housing market and investment opportunities.

The result? A so-called “Generation Rent” — not only unable to buy property, but also missing out on wealth accumulation entirely.

Part 5: The Way Forward with AiF Investment Strategies

So, what’s the solution? Your way forward lies in AiF’s investment strategies.

At AiF, we always remind people: If you don’t invest, you’ll fall behind financially.

Everything we’ve discussed today—the widening wealth gap in Canada—points to a harsh reality: relying only on earned income is no longer enough to keep up with inflation.

The only path forward is investment.

Beware of Get-Rich-Quick Schemes and Scams

But whenever you’re thinking about making money, you must keep this in mind: impatience and the desire to get rich quickly create the perfect breeding ground for scams.

With the rise of AI and rapid technological development, scams are only going to become more frequent and more sophisticated. In fact, they may already exist right in our communities and among the people around us, taking all kinds of forms—big and small.

That’s why it’s critical to understand: professional matters should be handled by professionals. Otherwise, it’s far too easy to fall into a scam.

AiF’s Experience and Advantages

AiF has been deeply rooted in the investment field for over 25 years. We follow strict standards: what should be done, what should not be done, and what must never be touched—all with clear boundaries.

We help clients leverage investment loans to channel their capital into the wave of the Fourth Industrial Revolution. With the arrival of the AI era, society’s wealth is undergoing a massive reshuffle, and we may even see an unprecedented wealth explosion in the near future.

Whether or not you can catch this “wealth express” depends entirely on whether you are willing to get on board.

The Difference Between Investing and Speculating

Wanting to make money is good—but you need clarity: trading individual stocks is not the right path.

Stock-picking is speculation. Buying a single stock is like buying a probability—it may rise, it may fall, and ultimately it’s uncertain. Even if you occasionally make a profit, you often end up giving it back to the market.

The Correct Approach: Guaranteed Funds + Investment Loans

The truly correct approach is to invest in public guaranteed funds.

Public guaranteed funds pool capital into leading funds in industry-leading sectors, reducing risk;

At the same time, these funds can be combined with Investment Loans.

As one of our advisors vividly puts it:

“It’s like borrowing a hen to lay eggs. You borrow someone else’s principal, but all the profit is yours.”

And only with public guaranteed funds can this model be truly realized.

Subscribe

Connect with

Login

I allow to create an account

When you login first time using a Social Login button, we collect your account public profile information shared by Social Login provider, based on your privacy settings. We also get your email address to automatically create an account for you in our website. Once your account is created, you'll be logged-in to this account.

DisagreeAgree

Connect with

I allow to create an account

When you login first time using a Social Login button, we collect your account public profile information shared by Social Login provider, based on your privacy settings. We also get your email address to automatically create an account for you in our website. Once your account is created, you'll be logged-in to this account.

DisagreeAgree

0 Comments

Inline Feedbacks

View all comments

You may also interested in

Real Estate Loss to Investment Gain: How David & Sarah Used Investment Loan Strategy to Double Assets| AiF Clients

See how David & Sarah used an investment loan strategy...

Read More

Leverage Investment Success: How Clients Achieved Over 200% Leverage Returns| AiF Clients

Discover how a Canadian family achieved 239% returns using strategic...

Read More

Canadian Soldier Achieves 204% ROI with Investment Loan and Segregated Fund| AiF Clients

Zack, a Canadian soldier in his 40s, turned limited savings...

Read More

From $100K to $520K: How a Millennial Actuary Couple Achieved a 154% Leveraged Return| AiF Clients

Discover how a millennial actuary couple used investment loans and...

Read More