加拿大统计局公布了2022年的...

Read MoreRecent Posts

- AiF观点 | 7大权重股对市场的影响 April 26, 2024

- AiF观点 | 加拿大统计局:中产年入7万, 你达标了吗? April 26, 2024

- S&P 500 posts best week since November, Nasdaq surges 2% Friday as Alphabet soars April 26, 2024

- AiF观点 | 核心通胀又涨了!意味着大家的支出又涨了! April 26, 2024

- S&P 500 and Nasdaq jump, boosted by Alphabet and Microsoft April 26, 2024

- 道指因美国经济增长放缓而下跌500点 | Ai Financial 财经日报 April 25, 2024

- AiF观点 | 加拿大打击房地产泡沫初见成效 April 24, 2024

- AiF观点 | 美联储:长期高利率不是坏事 April 24, 2024

- 特斯拉股价飙升12%,股市在盈利热潮中步履维艰 | Ai Financial 财经日报 April 24, 2024

- 五年翻倍的基金选择策略 | Ai Financial基金投资 April 24, 2024

- 纳斯达克连续第三天上涨,科技股涨势推动上涨 | Ai Financial 财经日报 April 24, 2024

- AiF观点 | 第四次工业革命的时代浪潮滚滚向前 April 23, 2024

- 标普500和纳斯达克大幅上涨,特斯拉开启“Magnificent 7”季报 | Ai Financial 财经日报 April 23, 2024

- AiF观点 | 财报季到了 April 23, 2024

- Stocks rise for a second day as earnings season ramps up, Dow up more than 100 points April 23, 2024

- Dow closes more than 200 points higher, S&P 500 snaps 6-day losing run as tech resurges April 22, 2024

- 【Weekly Recap】 Global dynamics, rate expectations, and earnings impact market volatility; Bull market persists, pullback brings investment opportunities April 22, 2024

- AiF观点 | 我们交的税去哪儿啦? April 22, 2024

- S&P 500 rises to start the week, tries to snap 6-day decline April 22, 2024

- Nasdaq falls more than 2% to post 6th straight losing day as Nvidia craters 10% April 19, 2024

Categories

一文看懂加拿大投资账户;买什么产品才能利益最大化? | Ai Financial 基金投资

- March 12, 2024

- March 12, 2024

Post Views: 1,082

Post Views: 1,082

加拿大居民享受多种注册账户福利,如RRSP的延税,TFSA的免税,还有新账户如FHSA等,那么多种投资账户,如何正确操作以高效利用账户福利,实现赚钱+节税?本文将全面介绍加拿大常用的投资储蓄账户,其用法及常见误区,并介绍适合这些账户持有的投资产品。

快速阅读链接

投资账户与常见误区

RRSP 注册退休储蓄账户

Registered Retirement Savings Plan is a Canadian account that can be used for savings and investments. Taxpayers have a high degree of autonomy within the rules set by the government, making it a savings plan. Generally, RRSP has two main advantages: first, the amount purchased in RRSP each year can be deducted from the current year's income tax; second, RRSP can help high-income individuals achieve deferred taxation.

Usually, you can easily open an RRSP account through financial institutions such as banks, investment companies, and trust companies. You have the option to contribute monthly, annually, or make a lump-sum purchase of RRSP.

As long as you have earned income, a Social Insurance Number (SIN), have filed taxes, and have available RRSP contribution room, Canadian permanent residents under the age of 71 are eligible to purchase RRSPs. Even if you're over 71, you can still contribute if your spouse is under 71, allowing you to enjoy the benefits of a Spousal RRSP.

我们可以将购买RRSP的目的分为短期目的和长期目的。

短期目的就是退税,这是非常直接有效的,让你拿回合理合法的退税。至于长期目的,则是养老,政府的最终目的是让有能力的人,也就是能购买得起RRSP的人,有自己的养老机制。

我们先来看短期目的-退税。

加拿大注册养老储蓄计划是在1957年由加拿大政府推出,为了鼓励加拿大人在有工作有收入的时候,进行一定的储蓄,然后到了退休后取出来,这样就有足够的收入过安逸的生活。由此,加拿大政府就推出了用RRSP来抵税的福利政策。

加拿大政府官网的定义告诉了我们RRSP账户是需要开户建立的;

购买RRSP账户的对象,可以是本人或者配偶SPOUSE或者同居伴侣COMMON-LAW PARTNER;

RRSP账户里面存入的钱,可以抵减收入,降低税阶,起到免税的作用。但是,RRSP在取出来的时候,有可能要上税。

那么,加拿大政府为什么要出台这样的福利政策呢?因为,加拿大政府没钱了!

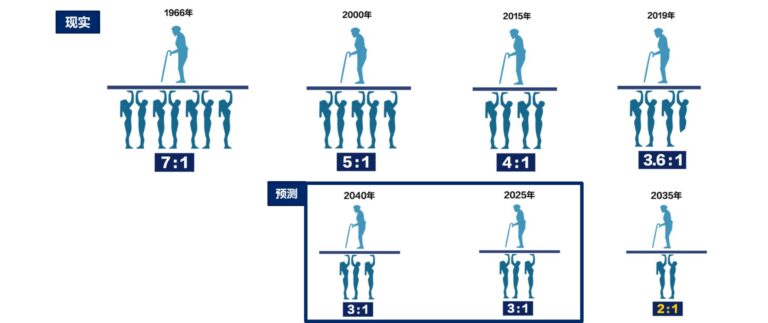

先看一下,历史上,缴纳CPP养老金的人数与领取养老金的人数的比例情况。

- 在1966年CPP刚建立的时候,7个上班人员养一位退休老人。

- 到2000年实际是5位上班族养1位老人。并且预计到2040年这个比例是3:1。

- 到了2015年,实际是4位上班族养1位老人。并且预计到2025年这个比例是3:1。已经比2000年當時的预测提前了15年到达3:1。

- 再到2019年,实际是3.6位上班族养1位老人。并且预计到2035年这个比例是2:1。这个变化的速度在不断加快。

- 所以,从养老体系来看,现在正在上班的人,每3.6人需要养活一位退休人士,而预计到2035年,就变成每两人供养一位退休人士。

不从数据,从现实的现象也可以看出,医疗的进步,养生产品,健康饮食,运动,医美的普及,使人类寿命大大延长。那么高龄的人士越来越多,又想要维持有品质的退休生活,怎么办呢?

为了降低这个供养人数减少的速度,国家采取了一系列的措施,其中,有一个非常明显的举措就是,增加CPP供款比例。

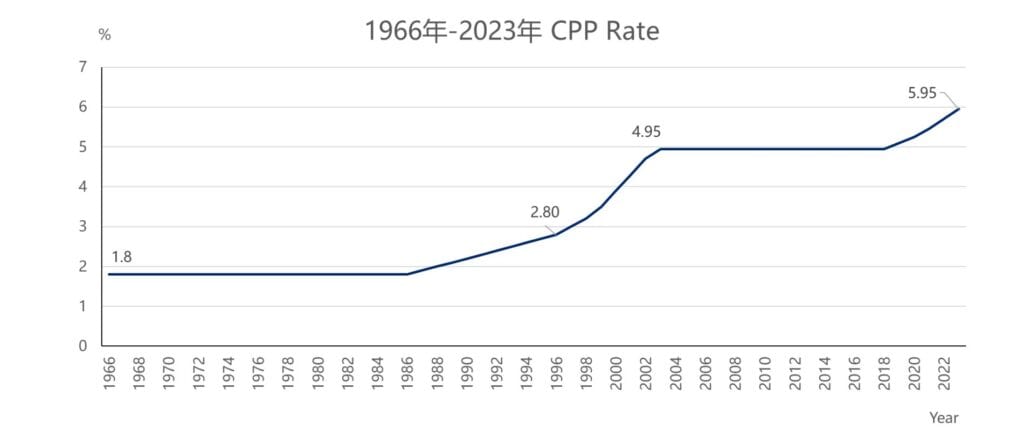

这是一张从1966年CPP成立开始,到去年2022年的缴纳CPP Rate的走势图,可以看出:

- 1966年到1986年CPP Rate一直维持在1.8%

- 到了上世纪80年代,发生CPP危机,所以每年开始上涨0.1%

- 1998年的时候,发现危机加剧,所以Rate的上涨幅度增加,幅度每年不等。

- 1999年CPPIB应运而生,CPP Investment Board (加拿大退休金計畫投資局),

这也是1999-2003以后,因为CPPIB运作投資良好,政府把rate固定在4.95% - 但是到了2019年,发现这个CPPIB可能也撑不住了,所以,又开始逐年增长。

- 到了2023年,CPP的上交Rate到了5.95%。說明他的投資並沒有真正解決問題, 我們只好自求多福-

这充分表明了,国家的养老金已经非常紧缺。如果老年人没有规划好自己的养老金,那么,这个养老金的负担就会落到自己的儿女身上,子女工作收入中要交的CPP一定会比我们自己年轻时候要交得多得多。

所以,我们购买RRSP的另外一个目的,是从长期来讲,为自己的养老作打算,是配合政府,规划自己未来舒适的养老生活。另一方面也为我们的子女减轻负担。

RRSP种类

购买RRSP的种类,常见的可以有三种:个人RRSP(Individual RRSP),配偶RRSP(Spousal RRSP),团体RRSP(Group RRSP)。它们的特点如下:

第一,个人RRSP(Individual RRSP)。顾名思义,就是以个人自己的名义开RRSP账户。这是最常见的RRSP形式,也是每个工薪人士最有可能购买的一种RRSP方式。只是在购买的时候,通常会考虑一个购买额度,否则,如果超出额度,每个月会向政府支付1%的罚金。

因为,RRSP作为一个政府CRA注册账户,与其它注册账户一样,是有额度限制的。

Subscribe to Ai Financial Newsletter

Sign up for our weekly stock market update and be the first to know about our webinars.

Newsletter Subscription

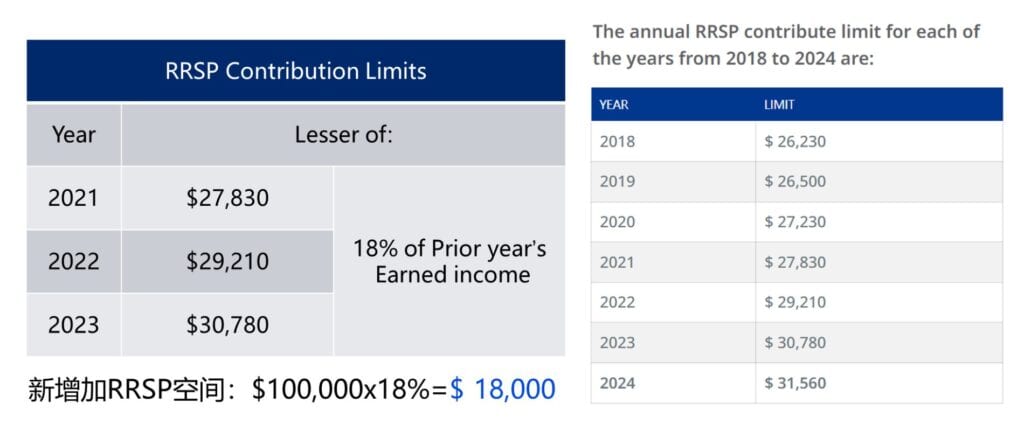

这个额度的计算公式是:RRSP当年的增长额度 = 上一年的年收入(Earned Income)X18%

也就是,个人在报税的时候,报给CRA的上一年的Earned Income,去乘以18%就得到了今年增加的RRSP的额度。没有报给税务局CRA的收入,不会被计入Earned Income。

例如:你2022年报了$100,000的收入,那你2023年的额度就是:$100,000 x 18%=$18,000,也就是,你在2023年又增加了$18,000的RRSP额度。但是,这个额度也不是无限的,政府规定了RRSP每年的CONTRIBUTION LIMITS,上表中列出了2021年到2023年,每年RRSP的限额,今年2023年的最高额度是$30,780。也就是,如果你的Earning Income是$20万,如果按照乘以18%的公式计算出来,应该是$36,000,但是政府只能让你购买最多是$30,780的RRSP。不能超出这个限额。

RRSP的额度是可以累积的,如果前面几年没有购买的额度,在以后的年份是可以使用购买的。而且购买的方式可以每个月供款,也可以一年一次供款,或者任何时候想买,只要有额度都可以购买。

第二,配偶RRSP(Spousal RRSP)。

配偶RRSP非常适合于夫妻间双方收入差距较大的情况,目的是通过此方法可以减少夫妻的总缴税额度。

这种RRSP类型适合于,夫妻之间收入差距比较大的情况。比如:先生收入是$15万,太太收入是$4万,那么,如果先生用自己的RRSP额度,为配偶购买了RRSP,这个RRSP就是Spousal RRSP。对于这个Spousal RRSP也是有一个限制的,就是3年之内不可以取款,如果3年之内,这个Spousal RRSP取出来,那么是要算作是先生的收入计税的。如果3年后取出来,就算作是太太的收入。

第三,团体RRSP(Group RRSP)。

团体RRSP,一般是公司给在职员工的一种养老福利。在加拿大,大型的国家机构如政府,医疗行业,教师工会,少数大型银行等都会有这类福利。那么,Group RRSP有哪些优势和劣势呢?

优势:如果你参与了公司的Group RRSP,那么,公司会承诺,你买一部分RRSP,那么公司就会配套支付一部分钱为你购买RRSP,但是,这个额度仍然是你自己的RRSP空间额度。

这个福利,公司是会设定一个上限的。有的公司是1:1配套,就是比如,你买4%,公司配套购买4%。而有的公司可能是1:0.5,那么你买4%,公司帮你购买2%。这个根据不同公司的福利情况而定。无论多少比例,这个都是公司给雇员的一个福利。

劣势:Group RRSP的投资标的非常有限,个人投资参与度很低,个人所能做的就是完成一份问卷调查,让Group RRSP的管理者了解你的风险承受能力,是保守的,激进型的等等,他们会根据你的问卷的结果,帮你作出选择。很少有公司让员工自己去选择投资标的。

另外,还有一个Group RRSP需要关注的就是,当你还在这家公司工作的时候,你是不能把这个Group RRSP转出来的,这个是锁定的,我们用另外 一个名词, LIRA,就是Locked in RRSP,除非你离开这个公司之后,你的公司给你开的Group RRSP就可以转出来。但是,你也不能直接转到自己的RRSP下面,只能转到一个Locked RRSP的账户下面。

这里介绍的这三种RRSP,供款的空间都是用的自己的RRSP额度,不管自己买的,还是公司买的,或者是给配偶买的,或是在多家机构开设账户,都会从自己的RRSP额度空间中扣除。所以,你购买的额度也不能超出自己的限额,否则,同样,每个月会支付给政府超额部分的1%的罚金。

TFSA 免税账户

Congratulations! Opening a TFSA account is extremely easy. TFSA stands for Tax-Free Savings Account, a type of account opened in an individual's name. As long as the applicant is at least 18 years old and has a valid Social Insurance Number (SIN), they can open a TFSA. This means that whether you are an international student with a study permit, a foreign worker with a work permit, or a Canadian resident with PR/Citizenship, you are eligible to open a TFSA and use it for investments.

You can use TFSA for various types of investments, including Segregated Funds, mutual funds, Exchange-Traded Funds (ETFs), stocks, bonds, and more.

While the deposits (principal) are not tax-free, the profits you earn from using TFSA for investments are completely tax-free. This includes capital gains, interest, dividends, and more.

The Canadian government sets an annual contribution limit for TFSA for each individual. In 2023, Canadian residents who are at least 18 years old can contribute up to a maximum of $6,500 to their TFSA account. The contribution limits vary each year, and here are the limits for previous years:

| Year | Limit |

|---|---|

|

2009 to 2012 |

$ 5,000 |

|

2013 and 2014 |

$ 5,500 |

|

2015 |

$ 10,000 |

|

2016 to 2018 |

$ 5,500 |

|

2019 to 2022 |

$ 6,000 |

|

2023 |

$ 6,500 |

|

2024 |

$ 7,000 |

Regarding TFSA Contribution Limits, its important to keep in mind:

- If you have remaining TFSA contribution room for the current year, you can carry it forward and accumulate it for use in the following years.

- If you turned 18 years old in 2009, even if you didn't file a personal income tax return, benefit application, or open a TFSA, your TFSA contribution room continues to grow each year.

- If you turned 18 years old after 2009, your TFSA contribution room starts accumulating from the year you turn 18, and it accumulates each year thereafter.

- The investment earnings and fluctuations in value of your TFSA investments won't affect your TFSA contribution room for the current year or the following years.

- A particularly advantageous aspect is that the capital appreciation and withdrawals from your TFSA account won't impact your eligibility for government benefits such as the Ontario Pension Plan, low-income subsidy benefits, federal tax credits, and more.

- Lastly, and most importantly, never exceed your contribution limit, as the tax agency will impose a penalty of 1% per month on the excess amount.

- Regarding your specific TFSA contribution limit, you can log in to your CRA account to check.

从CRA官网提供的案例中可以看出:

Joelle在4月和5月的前两次贡献使得她的2023年TFSA贡献空间降为零。由于她6月的提款直到下一年才会被加回到她的贡献空间中,她8月的贡献导致该月TFSA超额金额为$2,000。她9月的提款金额为$1,500,将被视为计算她在接下来的月份(10月)中最高超额TFSA金额的合格部分。超额TFSA金额$500将保留到年底,她将不得不在8月至12月的每个月支付1%的税。

Joelle的税款计算如下:

- 8月和9月每月的最高超额TFSA金额为$2,000。每月最高超额金额的1%税为$40($2,000 × 1% × 2个月)。

- 10月至12月每月的最高超额TFSA金额为$500。每月最高超额金额的1%税为$15($500 × 1% × 3个月)。

Joelle从她的TFSA中提款的金额将在2024年初被加到她的TFSA额度中。

而这个额度可以用多种方式查询:

- CRA网站,登录CRA网站(www.cra-arc.gc.ca),进入自己的 My Account,然后根据提示查询自己的TFSA额度。

- NOA,这是报完税后收到的CRA回执,这个回执会清楚的注明,您的TFSA使用情况。

- 拨打税务局电话 – 1-800-959-8281,这是一个语音电话,您先准备好去年报税的信息,然后可以根据提示进行查询。

- 最后,如果您是请会计师报税的,那么可以咨询您的会计师有关您的TFSA额度。

另外,TFSA账户还有一个重要的优点,就是提取方便。在TFSA账户中的资金可以随时提取使用,但是,政府规定,每年从TFSA账户中,因为取出钱,而腾出的额度空间,不能在当年重复使用,必须等到下一年,才能被重新激活使用。

RESP 教育储蓄账户

RESP is a Registered Education Savings Plan, a higher education subsidy program developed by the Canadian government. It aims to create an account for beneficiaries, who are youths under 17 years old and currently studying, to save for the expenses of completing higher education. As the contributions to the account accumulate interest and receive government grants, parents or subscribers who open an RESP account can significantly save on tuition fees.

Having an RESP investment account is a guarantee for a child's future education. As parents, we might cut costs in other areas, but education expenses for our children are non-negotiable.

The Do's and Don'ts of RESP Investments

Requirements for application

- When applying for an RESP investment account, the beneficiary must be:

- A Canadian resident and must be under 17 years of age.

- Have a Social Insurance Number (SIN).

- Preparing to attend an eligible post-secondary education program and requiring withdrawals from the RESP account to cover related expenses.

- If the beneficiary decides not to pursue higher education, the subscriber can:

Transfer the RESP account to another sibling.

If the subscriber or their spouse has available contribution room in their RRSP (Registered Retirement Savings Plan), funds can be transferred into the RRSP.

Take your time before withdrawing funds from the account while it's still valid. You can retain them temporarily to prevent any future needs. Typically, RESP accounts have a lifespan of 35 years.

If you wish to withdraw, you'll need to return the government grant portion to the government, and earnings will be subject to taxation plus a 20% penalty. Some RESP investment plans/types might have additional restrictions; it's advisable to inquire about these when opening the account.

- RESP contributions are limited to a lifetime maximum of $50,000 per beneficiary.

详细RESP信息请点击:Invest in RESP 或 有娃必看!利用RESP福利让孩子免费上大学

FHSA 免税首套住房储蓄账户

The Tax-Free First Home Savings Account (FHSA) was introduced in Canada on April 1, 2023, as a new registered plan following the Tax-Free Savings Account (TFSA). Designed to assist first-time homebuyers, FHSA combines the tax benefits of TFSA and RRSP. Contributions, investment income, and growth in FHSA are all tax-free, and withdrawals for a first home purchase are also tax-exempt, offering convenient and favorable financial support for homeownership dreams.

If you wish to open an FHSA account, you must meet at least...

- Be at least 18 years old and less than 71 years old by December 31 of the current year to qualify for opening an FHSA account.

- The account holder must be a resident of Canada.

- In the current year and the past four years, neither the account holder nor their spouse must have owned a property in Canada, and neither has designated any property owned by them or their spouse as their principal residence.

- The FHSA account can be held for a maximum of 15 years. Accounts can be opened through various financial institutions that offer TFSA and RRSP services, including banks, credit unions, life insurance companies, and Canadian trust companies.

三大税务优势账户对比

投资产品介绍 - 保本基金

以上所有账户都可以持有多种投资产品,例如:股票,债券,基金,ETF等。Ai Financial建议选择Segregated Funds 作为投资标的,凭借我们在行业中遥遥领先的投资视野及选基金能力,为客户带来五年翻倍的投资回报。

Segregated Funds, like Mutual Funds, are investments based on market dynamics. A large amount of money belonging to many people is invested in stocks, bonds or other securities under the operation of fund managers with the purpose of increasing the value of the entire pool of funds and creating returns for investors.

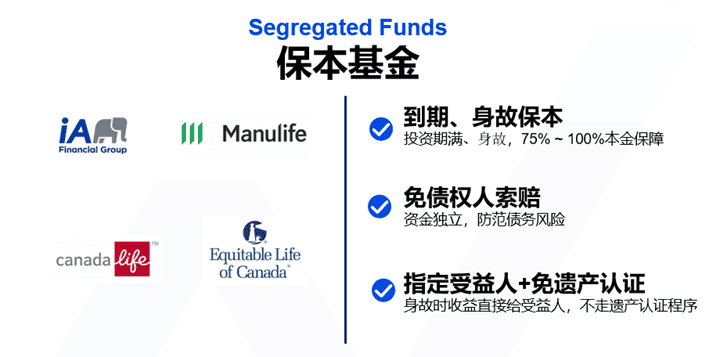

首先,保本基金可以提供到期保本和身故保本两种保本功能。到期保本意味着在一定的合同期限内(如20年或终身100岁)结束时,投资者将至少收回原始投资的75%或100%。升雇保本意味着即使基金出现亏损,投资者在合同期内也能至少获得75%的本金。这种保本功能是隔离基金的特点,与互惠基金不同。

其次,保本基金具有资金独立防范债务风险的功能。投资者在保本基金中的资金完全独立于其他资产,并且免受债权人的追索。这意味着在出现债务问题或法律纠纷时,投资者的资金是安全的,无法被债权人取走。

最后,投资者可以指定受益人,并且不需要经过漫长的遗产认证程序。这使得投资者可以在合同结束时直接将投资回报传给受益人,而不必支付昂贵的遗产认证费用。

尽管保本基金的管理费可能略高于互惠基金,但考虑到保本基金提供的额外保障和便利性,投资者应该权衡费用和收益,并认识到后期可能避免的大额支出。

银行和基金公司合作发行的互惠基金与保本基金有许多相似之处。例如,交易简便透明,费用较低,入门门槛低,您可以轻松地投资数额从50到100不等,甚至更多。我们稍后将展示一个真实的开户案例。

投资公共基金本身已经实现了投资的分散。选取龙头板块的龙头企业,我们的基金组合已经包括了数十甚至上百家企业,这样的分散程度已经足够。因此,投资者不必再次将资金分散投资在其他方向上,因为这样做可能会导致收益不佳甚至亏损。

尽管互惠基金和保本基金在公开透明度和资金方面相似,但选择保本基金还有其他优势。例如,保本基金具有很强的流动性,您可以随时提取资金,这在家庭现金流不足时非常重要。而且,保本基金可以提供税务便利,您可以通过定期投资来积累财富。

当然,保本基金可能会有稍高的管理费,但是您不应该只考虑费用,而忽略了投资标的的质量和长期收益。便宜的东西未必好,投资是一个需要谨慎考虑的过程。

最后,要强调的是,保本基金并非用于财富传承,而是真正的投资产品。它们提供了诸多特性,使得您可以安心地进行长期投资。

家庭无论资金多少,都可以通过加拿大注册账户(如TFSA、RSP以及教育基金等)进行投资。您可以在这些账户中进行投资,包括注册账户和非注册账户。举例来说,您可以将资金存入注册账户或非注册账户,并在您名下进行投资。

此外,保本基金具有一个重要的功能,即您可以通过投资贷款利用杠杆进行保本基金的投资。您可以最大化投资本金,并将其作为未来退休的储备。利用基金的这种特性,随着时间的推移,您将在10年或20年后看到账户中积累了可观的财富。这是因为您通过使用杠杆增加了投资本金,从而确保在退休时拥有充裕的资金。

在投资贷款和自有资金的双重投资下,我们可以帮助您最大化投资本金,并获得最佳收益。考虑到通货膨胀和长寿的因素,尤其是对于70后和85后的家庭来说,至少需要拥有百万级的投资资金才能实现退休财务自由。这样的投资资金才能够在未来十年、十五年或二十年后帮助您积累到足够的财富。

因此,不要等到晚年才开始规划退休金,因为这样可能为您的退休生活带来不必要的困难。现在就开始规划退休金非常重要,以确保您的未来财务安全。

Ai Financial Funds Investing - You fulfill your dreams, we cover your bills

Ai Financial is a leading Canadian Fin-Techfund investmentservice provider. We leverage cutting-edge technology to adhere toValue Investing principles,aiming to drive reform in Canada's pension system and enable more people to live better lives through financial investment.

Ai Financial has a background in financial compliance and anti-money laundering (AML). Through collaborations with banks, funds, and insurance companies, we select fund products suitable for clients and managevarious investment accountssuch as TFSA and RRSP. Additionally, we assist clients in applying for unique CanadianInvestment Loan, facilitating early attainment of financial freedom.

RELATED READING

Subscribe to Ai Financial Newsletter

Sign up for our weekly stock market update and be the first to know about our webinars.